AI and the data center impact in 2026

The AI boom in 2026 is no longer just a software story.

It is now a power story, a grid story, a construction story, a water story and a capital-allocation story. The data center layer sitting underneath AI has become one of the most important physical bottlenecks in the whole technology economy. What looked like a cloud computing expansion cycle a few years ago now looks more like an infrastructure supercycle. The newest 2026 research points in the same direction again and again - AI demand is forcing much bigger spending on data centers, much faster growth in electricity consumption, much tougher competition for power connections and much tighter capacity in major markets.

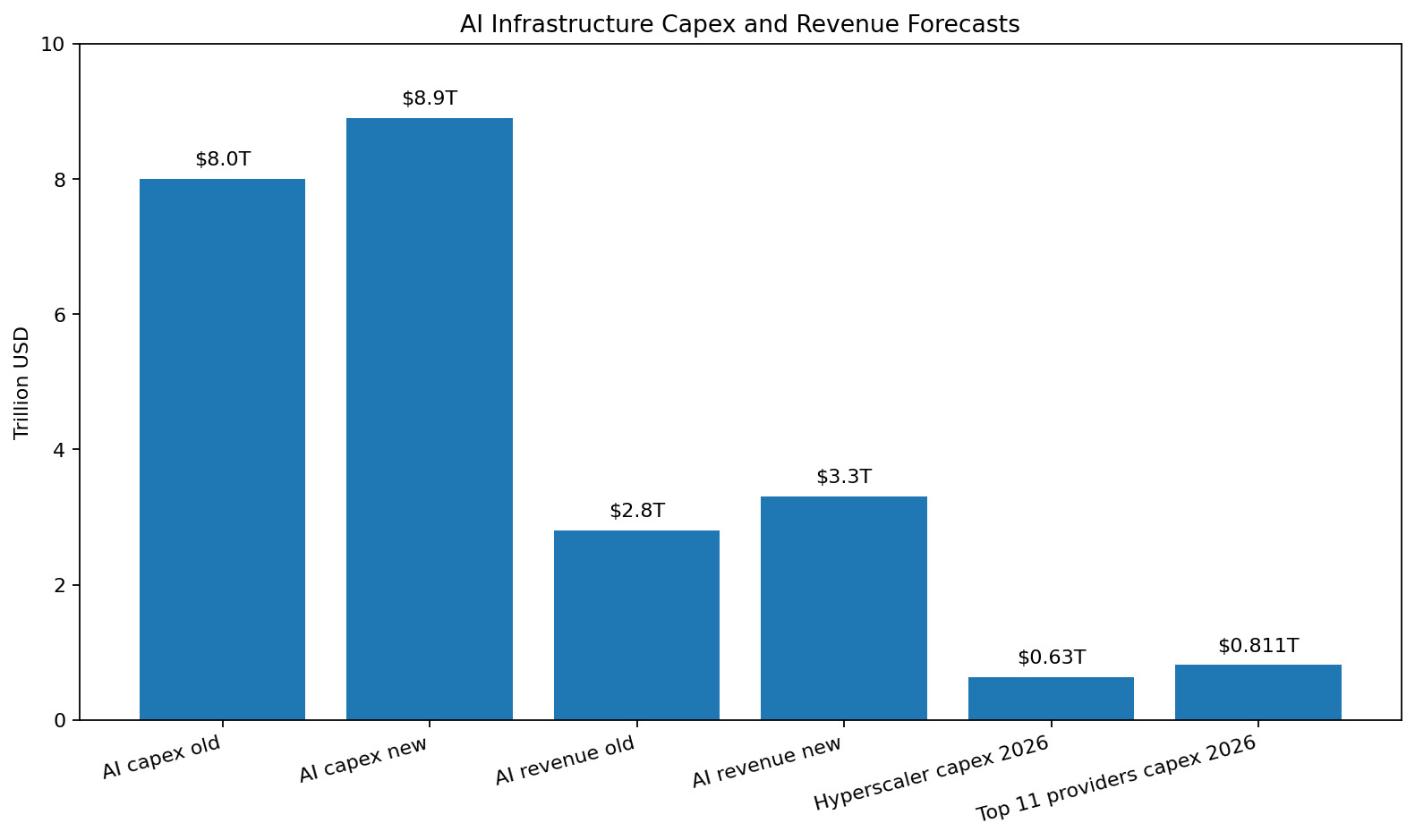

The scale is huge. Citigroup raised its forecast for global AI related capital expenditure in 2026 to 2030 to $8.9 trillion, up from $8 trillion and lifted its AI revenue forecast for the same period to $3.3 trillion from $2.8 trillion. Reuters also reported that hyperscalers such as Amazon, Microsoft, Alphabet and Meta are expected to spend more than $630 billion in capital expenditure in 2026 alone, while a broader Morgan Stanley estimate puts 2026 capex for the top 11 cloud and infrastructure providers at $811 billion.

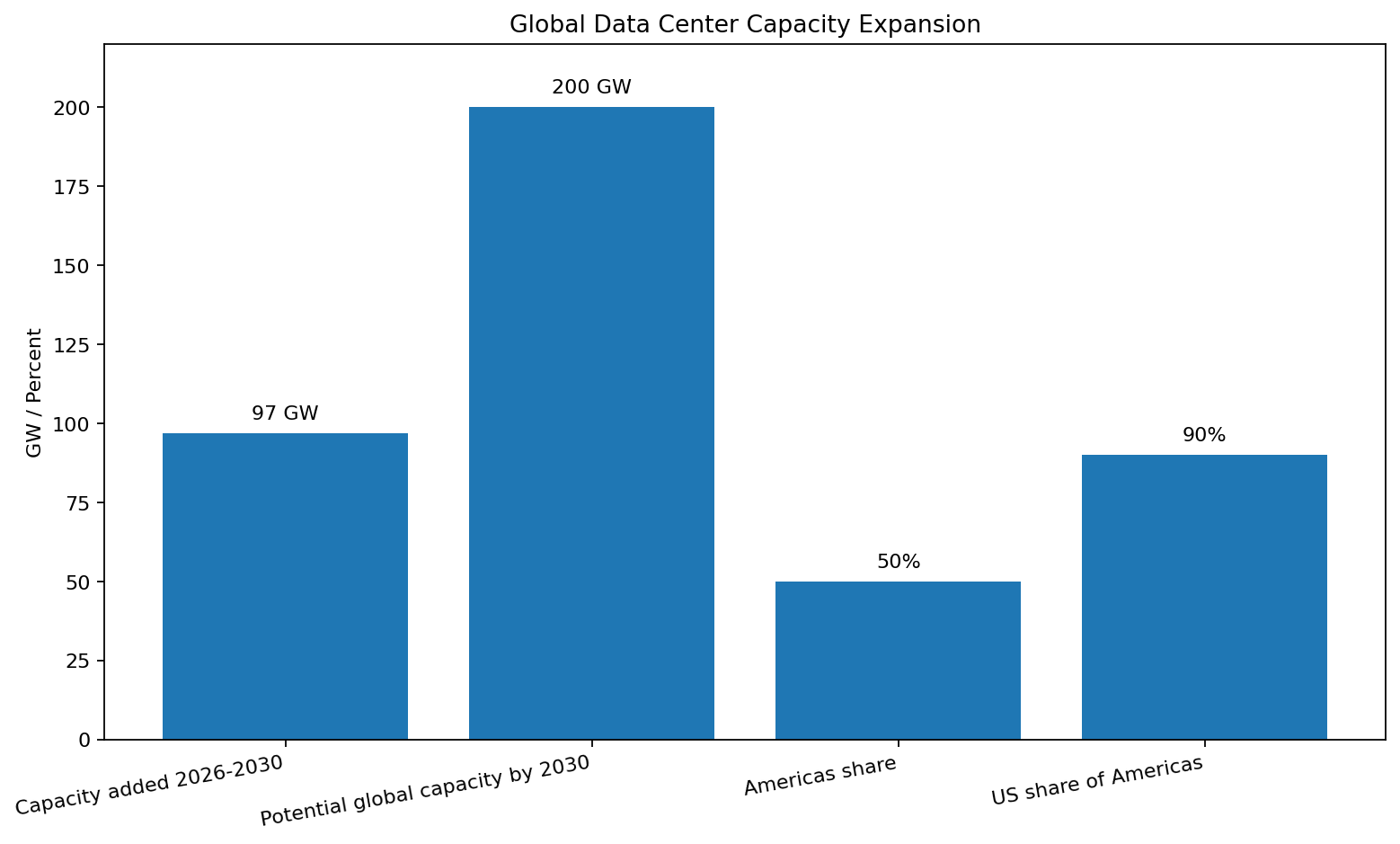

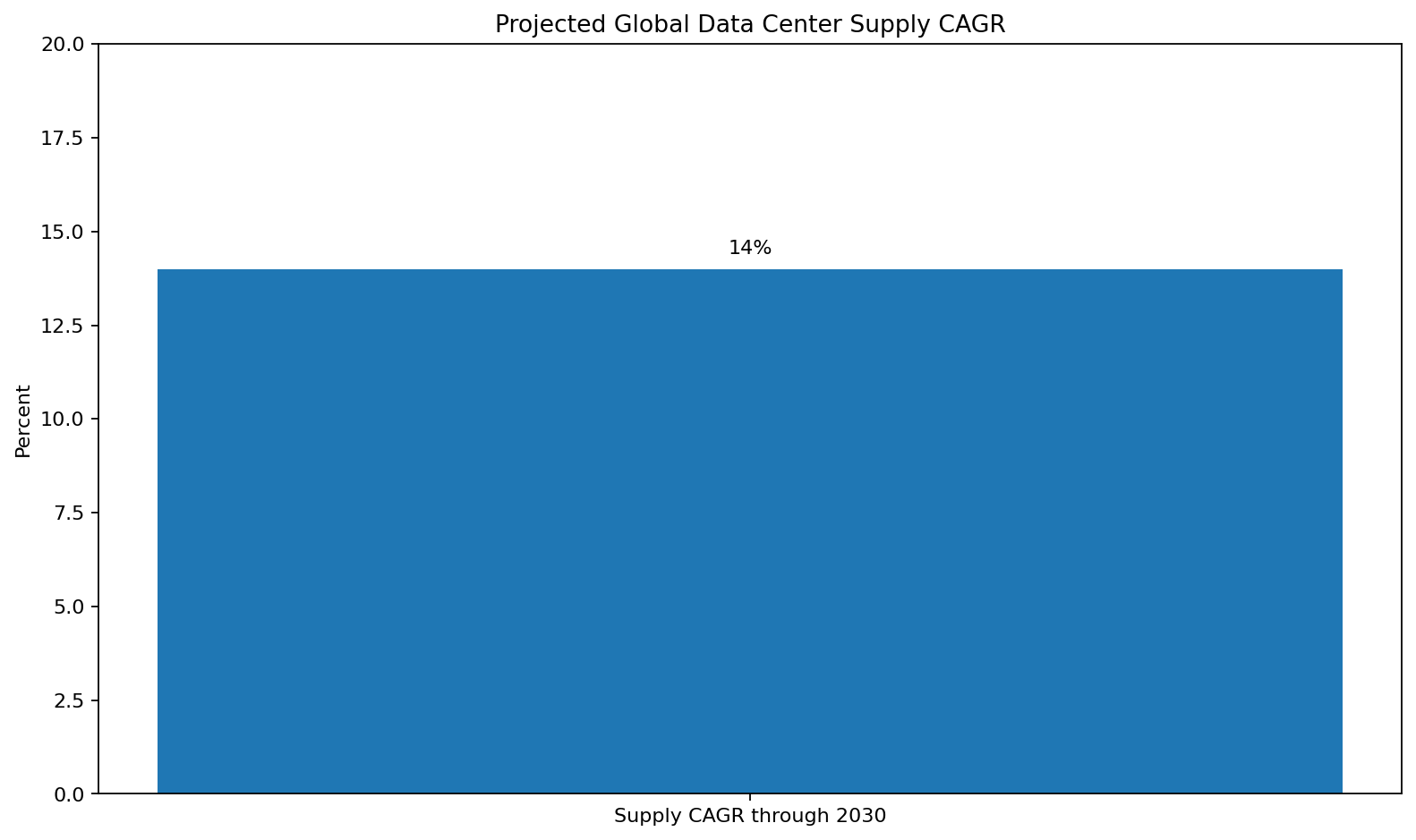

That money is flowing into a data center market that is expanding at extraordinary speed. JLL’s 2026 Global Data Center Outlook says the sector is projected to add 97 gigawatts of capacity between 2026 and 2030, effectively doubling in size with global capacity potentially reaching 200 GW by 2030. JLL also projects a 14% global supply CAGR through 2030 with the Americas representing about 50% of global capacity and the United States accounting for about 90% of capacity in the Americas.

That is the physical footprint of the AI race.

AI is sharply increasing electricity demand

The most important impact may be energy.

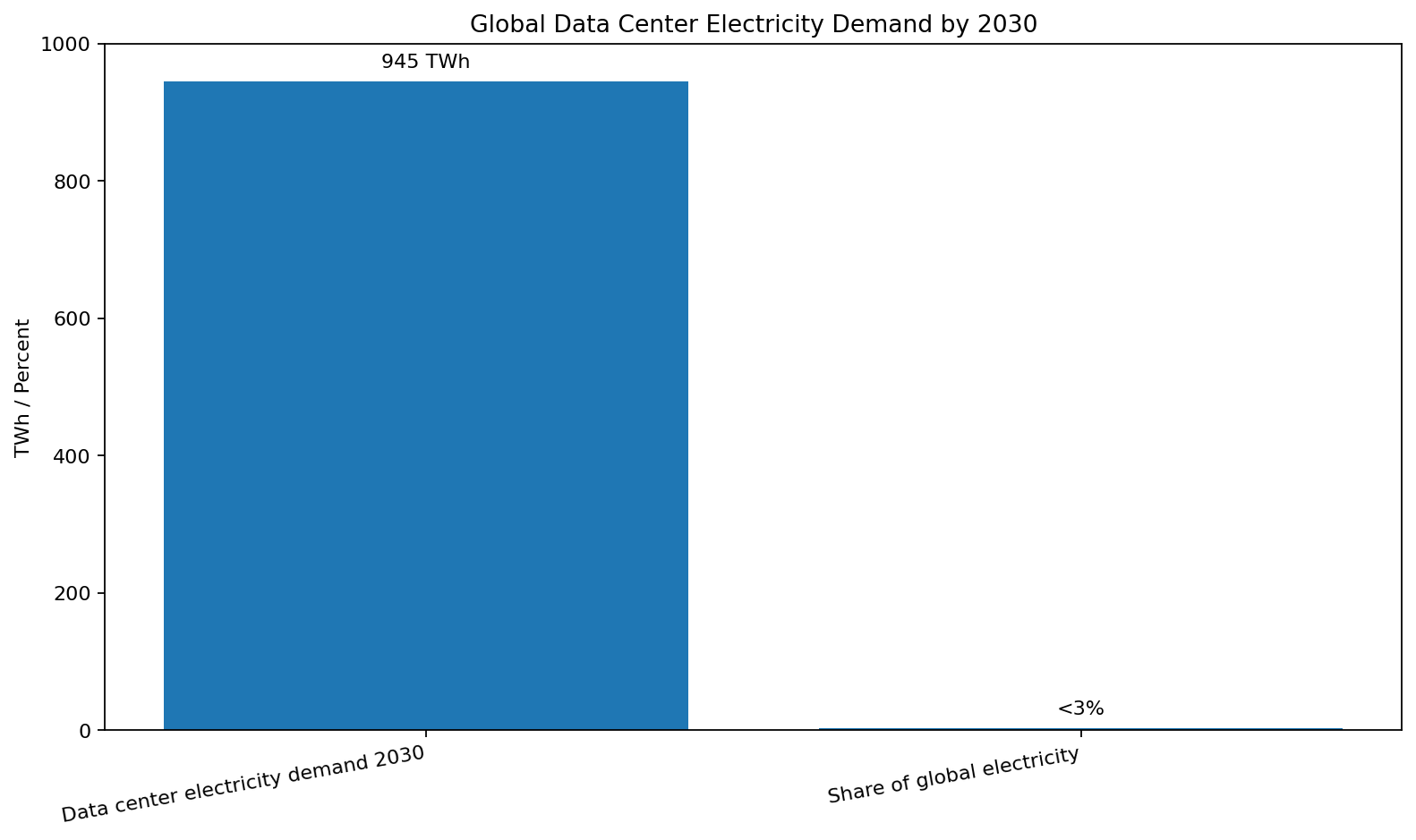

The IEA’s latest work says global electricity consumption from data centers is projected to double to around 945 TWh by 2030 in its base case, reaching just under 3% of total global electricity consumption. From 2024 to 2030, data center electricity use is expected to grow by around 15% per year, more than four times faster than the growth rate of electricity demand from all other sectors. The IEA also says accelerated servers, which are mainly driven by AI adoption are projected to grow electricity consumption by 30% annually and those accelerated systems account for almost half of the net increase in global data center electricity demand.

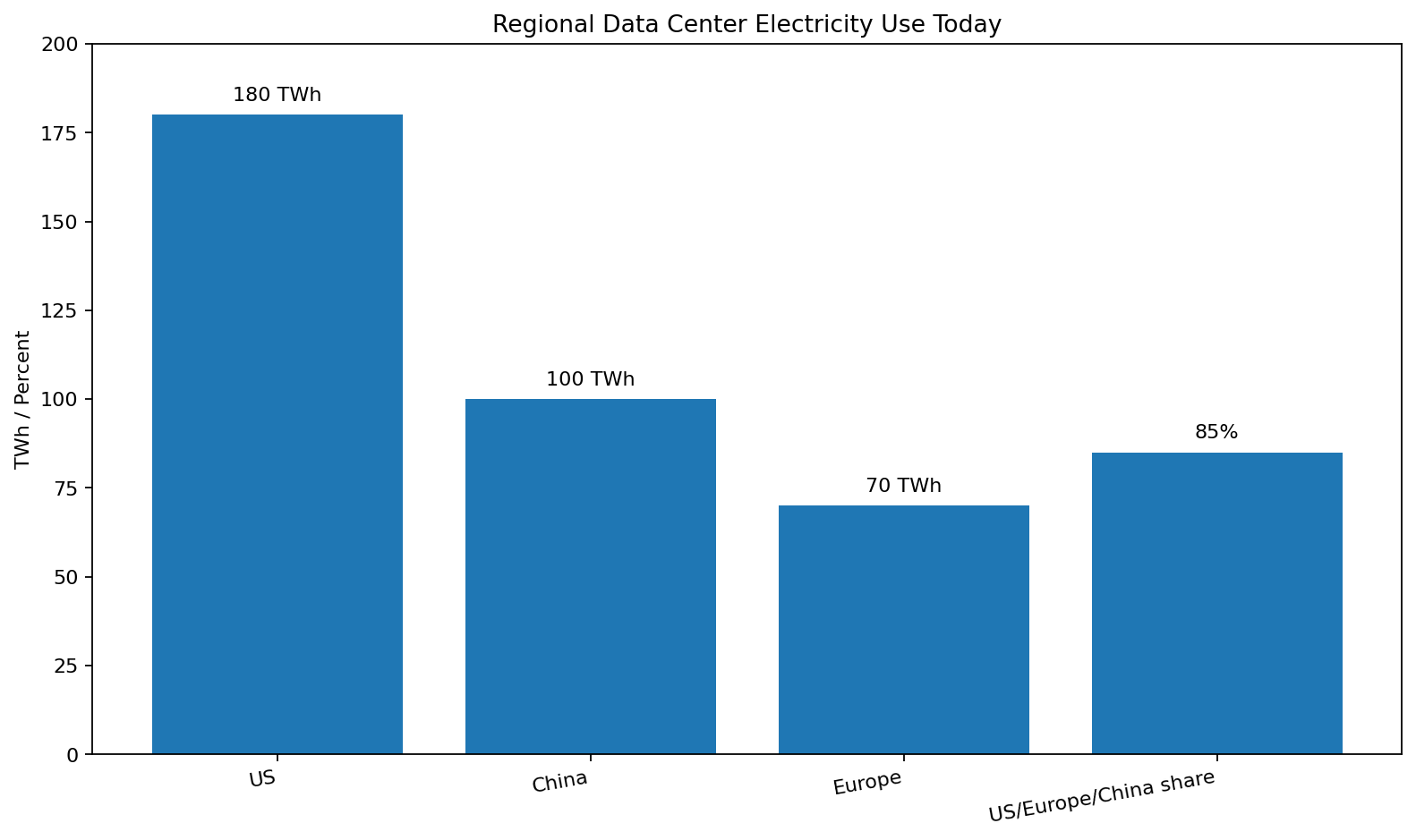

That growth is not evenly spread. The IEA says the United States, Europe and China account for around 85% of global electricity consumption from data centers today. In 2024, data centers consumed around 180 TWh in the United States, nearly 45% of global total and more than 4% of all US electricity consumption. China accounted for around 100 TWh and about 25% of global data center electricity consumption, while Europe accounted for roughly 70 TWh.

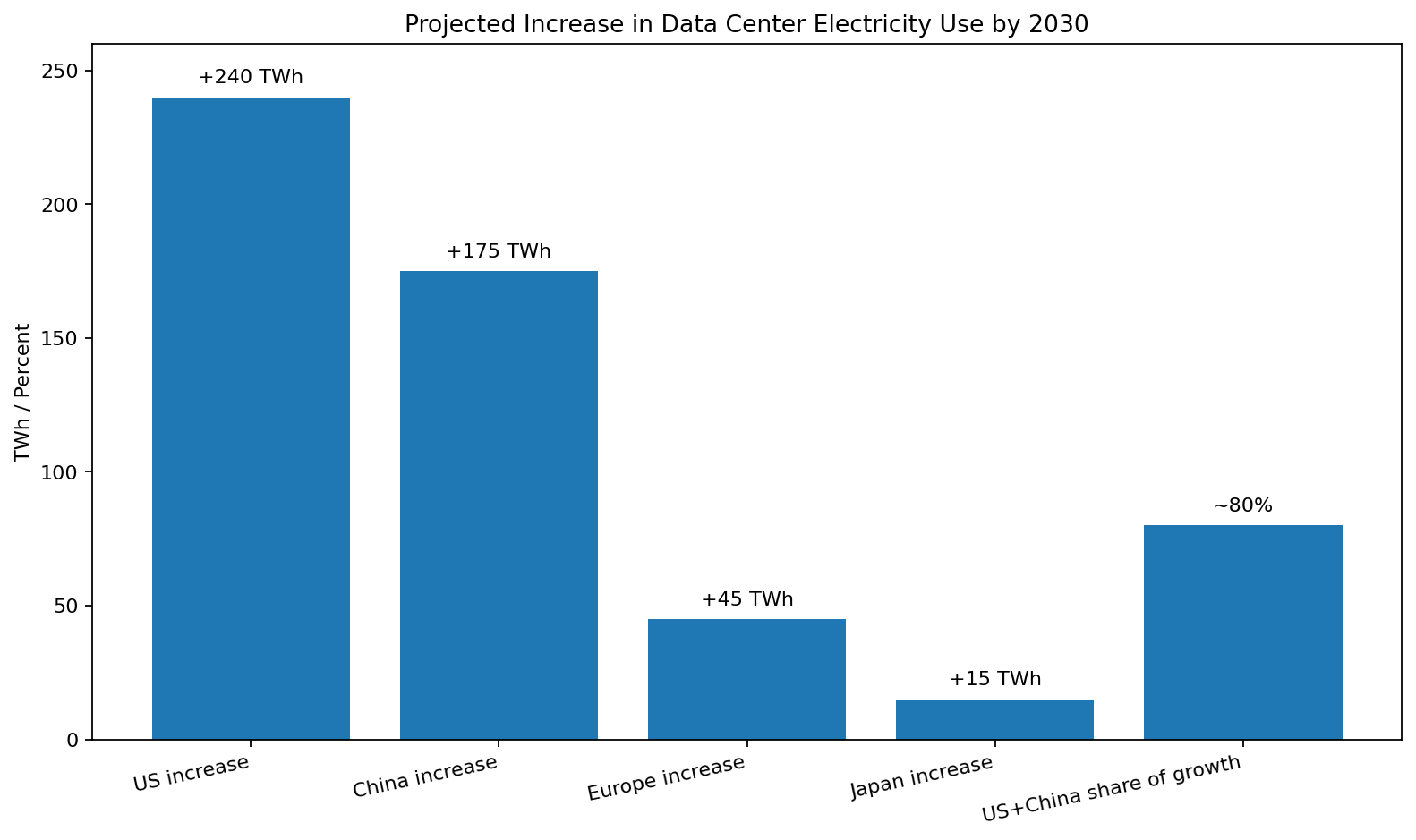

Looking ahead, the US and China dominate the next wave too. The IEA projects that between 2024 and 2030, US data center electricity use rises by around 240 TWh, up 130%, while China rises by around 175 TWh, up 170%. Europe grows by more than 45 TWh, or about 70% and Japan by around 15 TWh, or about 80%. Together, the US and China account for nearly 80% of global growth in data center electricity consumption through 2030.

This is why AI has become a genuine power system issue rather than a niche tech issue.

The bottleneck is increasingly power, not just land or fiber

One of the clearest 2026 themes is that the real constraint on data center growth is shifting.

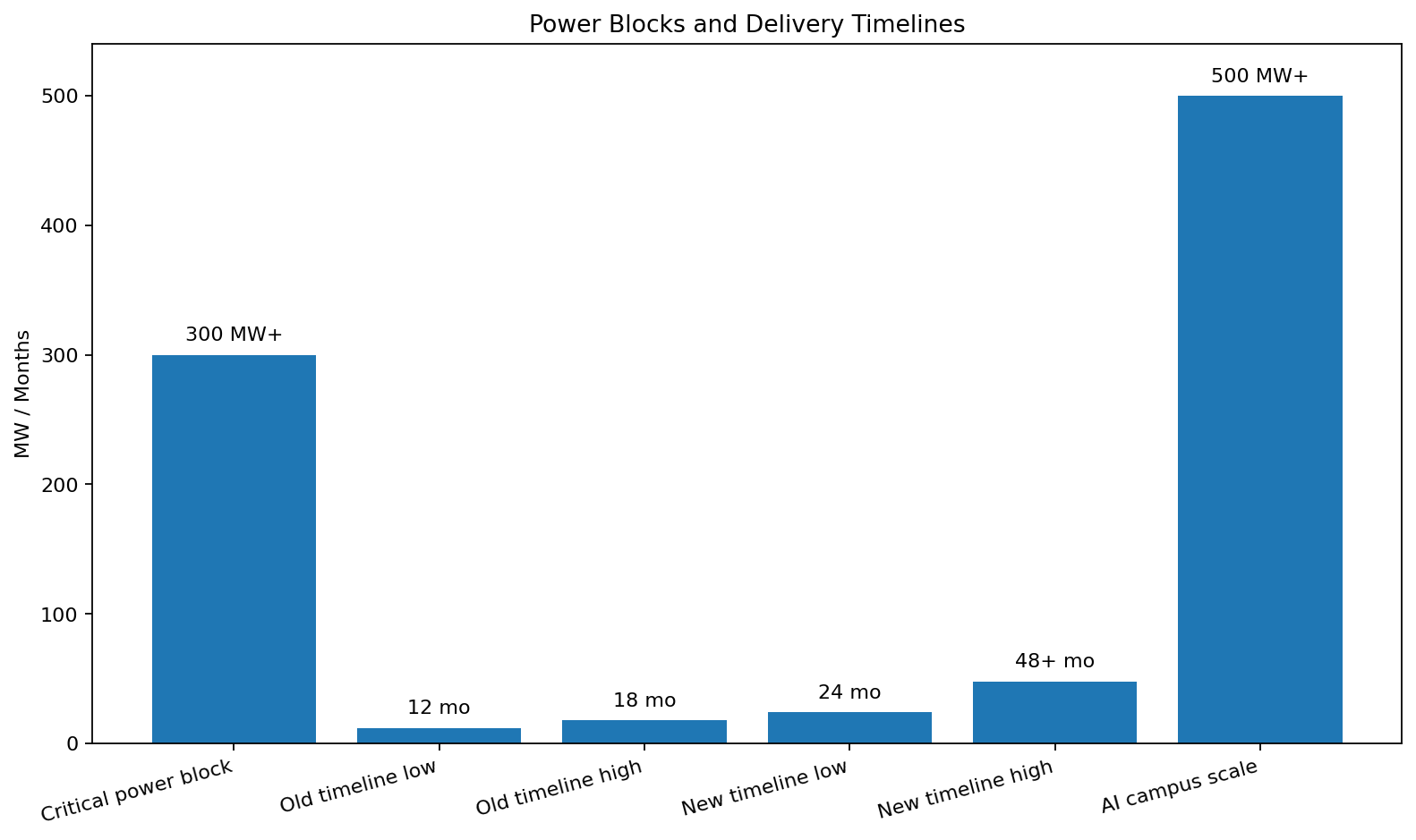

CBRE says US data center demand continues to hit unprecedented levels, with 2026 on track for a new leasing record but new supply is becoming much harder to deliver because the ability to secure 300 MW plus power deliveries within 36 months now matters more than connectivity. CBRE adds that the old 12 to 18 month timeline for sub 50 MW buildings no longer applies because 500 MW plus AI campuses have pushed delivery into multi year schedules. Any need for new high voltage transmission or incremental generation can stretch timelines to 24, 36 or even 48+ months.

Uptime Institute is making the same point more bluntly. Its 2026 predictions say developers will not outrun the power shortage and that AI driven load growth will intensify pressure on already constrained grids. Bloomberg Energy’s 2026 Data Center Power Report similarly says power availability is now driving a geographic reallocation of data center growth and that an increasing share of campuses are expected to exceed gigawatt scale. It says Texas is poised to become the leading US data center market within three years while some legacy markets are expected to lose more than half their relative share.

That is a major shift. For years, data center conversations centered on latency, tax incentives and network density. In 2026 access to power is becoming the main strategic filter.

Capacity is so tight that vacancy is near the floor

This pressure is showing up clearly in market vacancy data.

CBRE says the overall vacancy rate in North America’s primary data center markets fell to a record low 1.4% at year end 2025. Primary market supply still increased by 36% year over year to 9,432 MW but net absorption hit a record 2,497.6 MW beating the previous record of 1,809.5 MW in 2024. Northern Virginia alone absorbed 1,102 MW, while Dallas absorbed 470.8 MW. At the same time, the average asking rate for a 250 to 500 kilowatt requirement rose 6.5% year over year to $195.94 per kW per month.

JLL’s global view is similar. Its 2026 outlook says demand is projected to keep pace with supply growth and maintain a sub 10% global vacancy rate even as the industry scales rapidly. In the UK, CBRE says London’s data center take up is forecast to reach 189 MW in 2026 against 180 MW of new supply making 2026 the fifth straight year that take up outpaces new delivery. It projects a London vacancy rate of 5.9% by the end of 2026 which would be a record low.

This kind of tightness is important because AI workloads often need very large blocks of power and space very quickly. When vacancy is already minimal, preleasing and long lead times become standard rather than exceptional.

AI is turning cloud growth into infrastructure growth

Cloud demand is also feeding the same trend.

Synergy Research says enterprise spending on cloud infrastructure services reached $129 billion in Q1 2026, up by more than $35 billion year over year, representing an annualized revenue run rate of over half a trillion dollars. That was a 35% year on year growth rate, the highest since the end of 2021 and Synergy explicitly says GenAI is driving major changes in cloud market dynamics. Amazon’s worldwide market share was 28%, Microsoft’s 21% and Google’s 14% in Q1 2026.

This matters because AI infrastructure demand does not only come from model developers. It also comes from enterprise customers renting AI capacity indirectly through cloud platforms. So even when a company is “just using cloud AI,” the physical effect often still lands in a hyperscale data center somewhere.

The energy mix is improving but fossil fuels still matter

One of the biggest misunderstandings in this debate is that AI related data center growth will be powered entirely by clean energy in the near term.

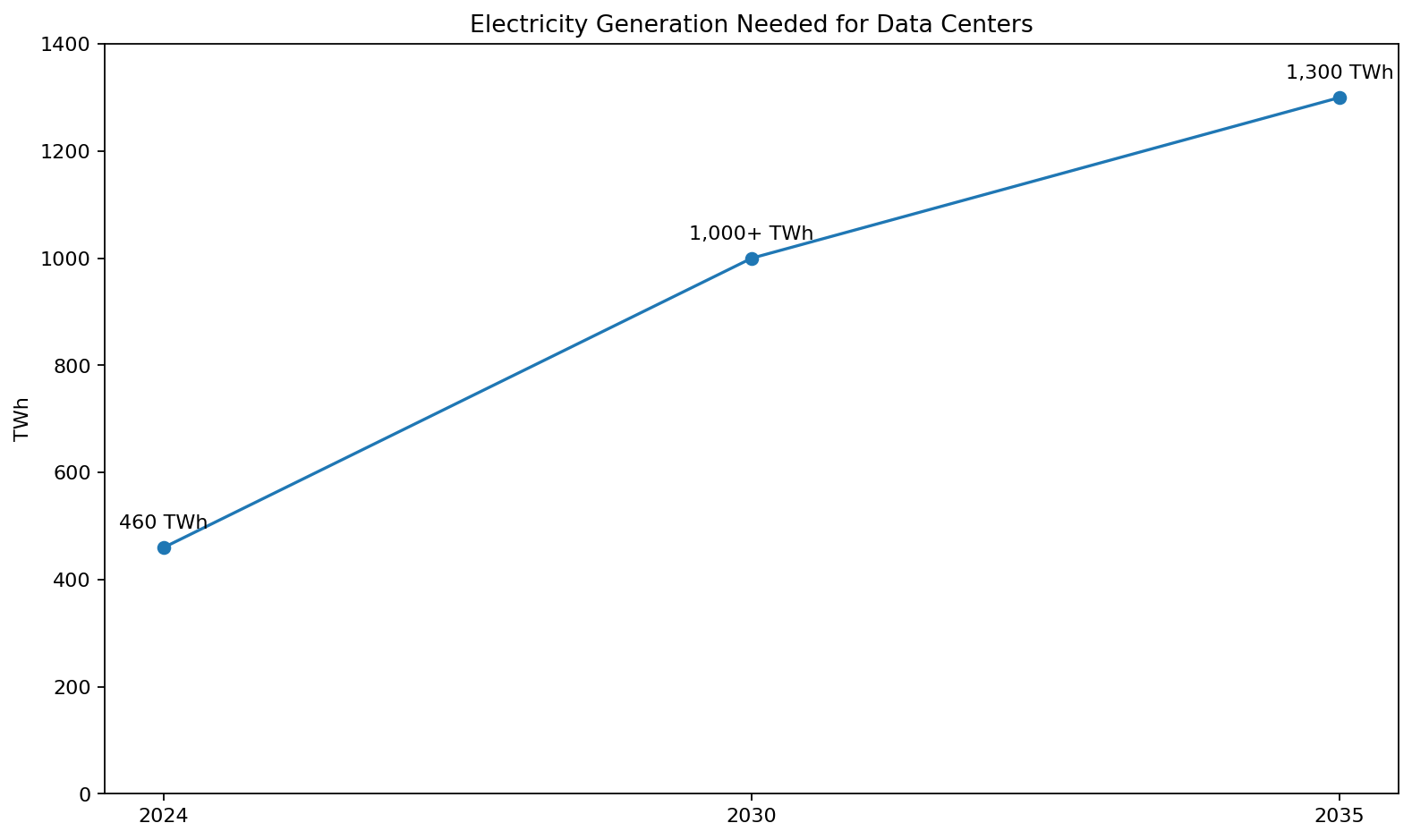

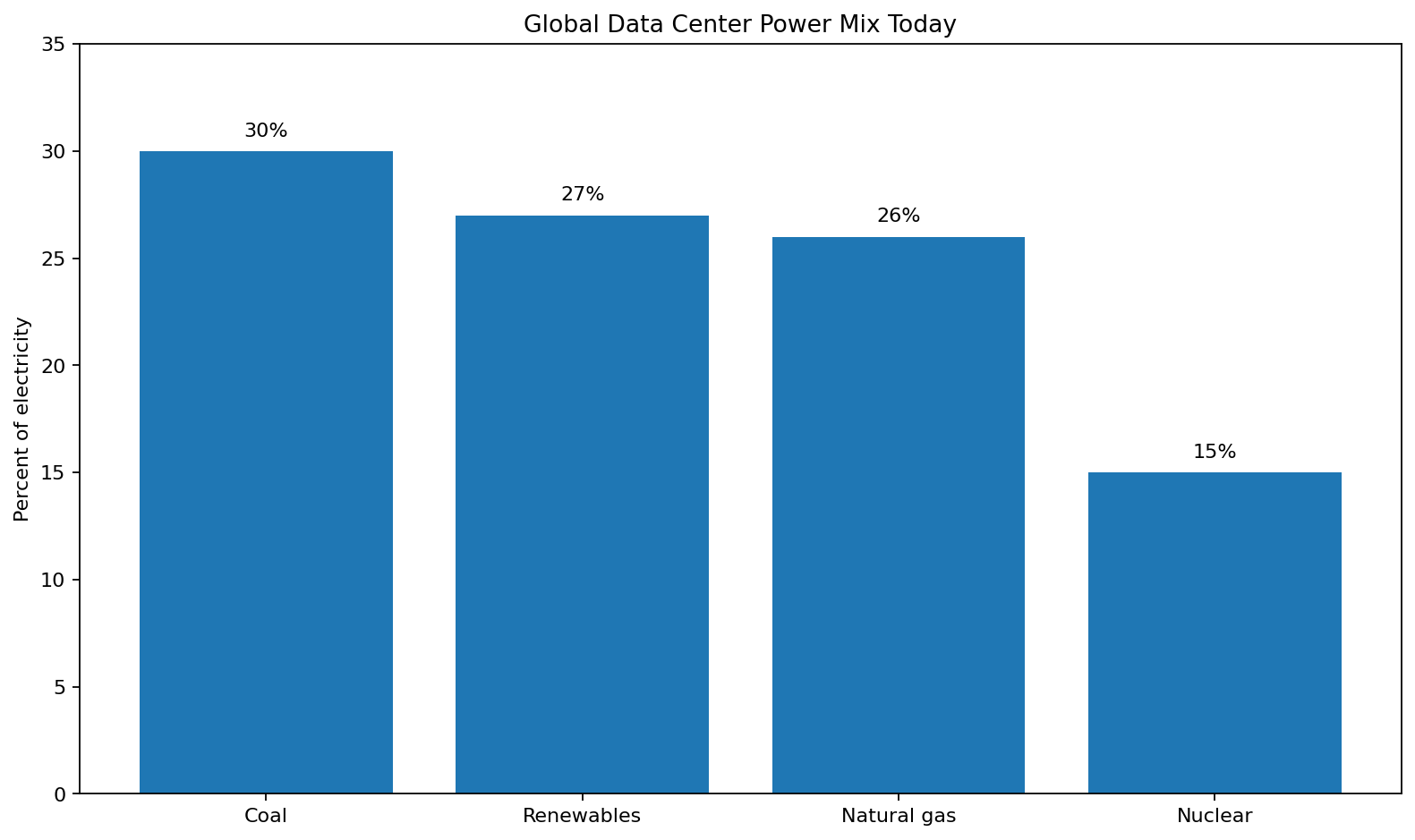

The IEA says global electricity generation to supply data centers is projected to grow from 460 TWh in 2024 to over 1,000 TWh by 2030 and 1,300 TWh by 2035 in its base case. Renewables are expected to meet nearly half of the additional demand through 2030, making them the fastest growing source. But the IEA also says natural gas and coal together are expected to meet over 40% of the additional electricity demand from data centers until 2030. Today, coal supplies about 30% of electricity physically consumed by data centers globally, renewables about 27%, natural gas 26% and nuclear 15%.

The regional picture is even more revealing. In the United States, natural gas already supplies over 40% of the electricity used by data centers, with renewables at 24%, nuclear around 20% and coal around 15%. The IEA expects natural gas to be the largest source of additional US supply through 2030 adding over 130 TWh, while renewables add about 110 TWh. In China, coal currently provides nearly 70% of electricity consumed by data centers. Europe looks cleaner, with renewables and nuclear together expected to supply 85% of additional data center electricity demand by 2030.

So the short version is this: AI is accelerating clean power procurement but it is also increasing near term reliance on fossil generation where grids are tight.

Emissions are rising before they flatten

That leads naturally to carbon.

The IEA projects that CO2 emissions from electricity generation for data centers will peak at around 320 million tonnes by 2030, then ease slightly to around 300 million tonnes by 2035 in the base case. Even then, data centers remain less than 1% of total global CO2 emissions. That sounds manageable globally but it hides the local stress problem - data centers may be a small share of global emissions yet they can be a very large load in specific grid zones.

That local concentration is really the key issue. The IEA notes that while data center electricity demand growth accounts for less than 10% of global electricity demand growth from 2024 to 2030, data centers tend to cluster geographically, making grid integration much harder than the global averages imply.

Water is becoming a much bigger part of the conversation

Power is the headline constraint but water is rising fast as a second order issue.

A recent UK government commissioned report says the global data center sector already consumes over 560 billion litres of water annually and could reach as much as 1,200 billion litres by 2030. The report also notes that a 100 MW hyperscale facility can consume around 2.5 billion litres of water per year, roughly equivalent to the needs of 80,000 people. It further says AI tools could indirectly lead to global water withdrawals of 4.2 billion to 6.6 billion cubic metres by 2027.

This matters because AI oriented data centers increasingly use high density compute which can raise cooling intensity unless operators shift to better thermal designs, reclaimed water, liquid cooling or different siting strategies. Water is still less discussed than electricity but in 2026 it is clearly moving from a side note to a planning issue.

The data center buildout is now a genuine industrial race

This is also becoming a huge industrial opportunity.

McKinsey describes the global AI data center buildout as a $7 trillion race with industrial companies competing to supply power equipment, cooling systems, electrical gear, controls and modular infrastructure. JLL separately describes a $3+ trillion investment supercycle supporting nearly 100 GW of new capacity and a $500 billion technology opportunity across power, cooling, infrastructure and management.

This is why AI’s data center impact stretches well beyond tech firms. It affects utilities, turbine makers, switchgear manufacturers, transformer supply chains, engineering firms, EPC contractors, real estate investors, chipmakers, cooling vendors and local governments competing for projects.

2026 is the year AI infrastructure meets physical reality

The big theme running through all the 2026 data is that AI demand is colliding with the real world pace of infrastructure.

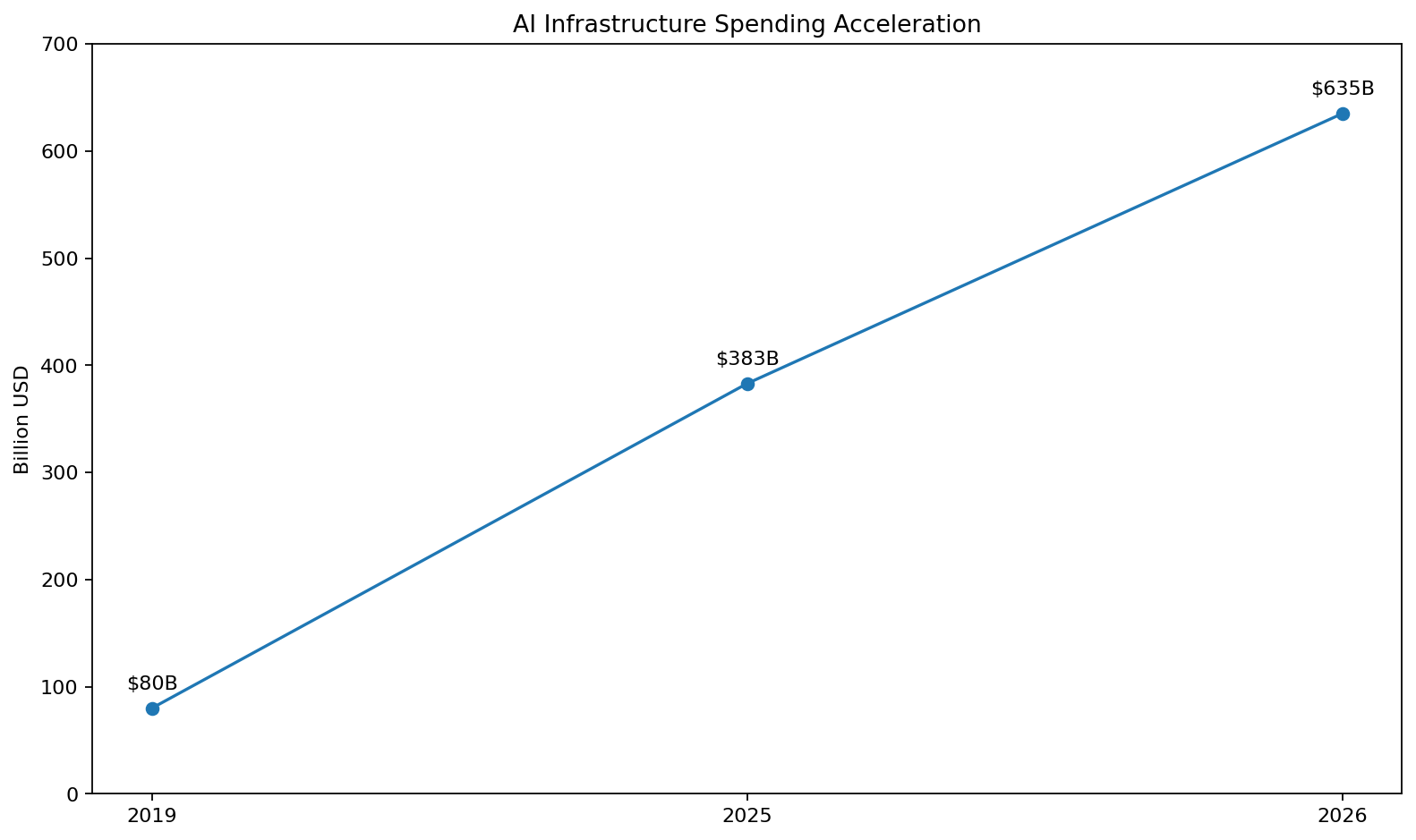

The money is there. The demand is there. The software adoption is there. But power, interconnection timelines, construction complexity, vacancy shortages and water constraints are now dictating how fast the AI buildout can actually happen. Reuters captured that tension well when it noted that planned 2026 spending of roughly $635 billion on AI infrastructure faces a serious energy cost test up from $383 billion the prior year and just $80 billion in 2019.

This is the most important point for anyone writing about AI and data centers in 2026.

AI is no longer mainly limited by algorithms.

It is increasingly limited by substations, turbines, transmission, transformers, cooling systems, planning approvals, construction schedules and regional electricity prices. The next phase of AI growth will belong not just to the companies with the best models, but to the ones that can secure the best physical infrastructure.

Sources

https://www.iea.org/reports/energy-and-ai/energy-demand-from-ai

https://www.iea.org/reports/energy-and-ai/energy-supply-for-ai

https://iea.blob.core.windows.net/assets/de9dea13-b07d-42c5-a398-d1b3ae17d866/EnergyandAI.pdf

https://www.iea.org/reports/electricity-2026

https://www.jll.com/en-uk/insights/market-outlook/data-center-outlook

https://www.cbre.com/insights/books/us-real-estate-market-outlook-2026/data-centers

https://www.cbre.com/insights/books/north-america-data-center-trends-h2-2025

https://www.cbre.co.uk/insights/books/uk-real-estate-market-outlook-2026/data-centres

https://www.bloomenergy.com/wp-content/uploads/2026-power-report.pdf