Economic potential of AI in 2026

AI’s economic potential in 2026 looks enormous but the most credible way to describe it is in layers.

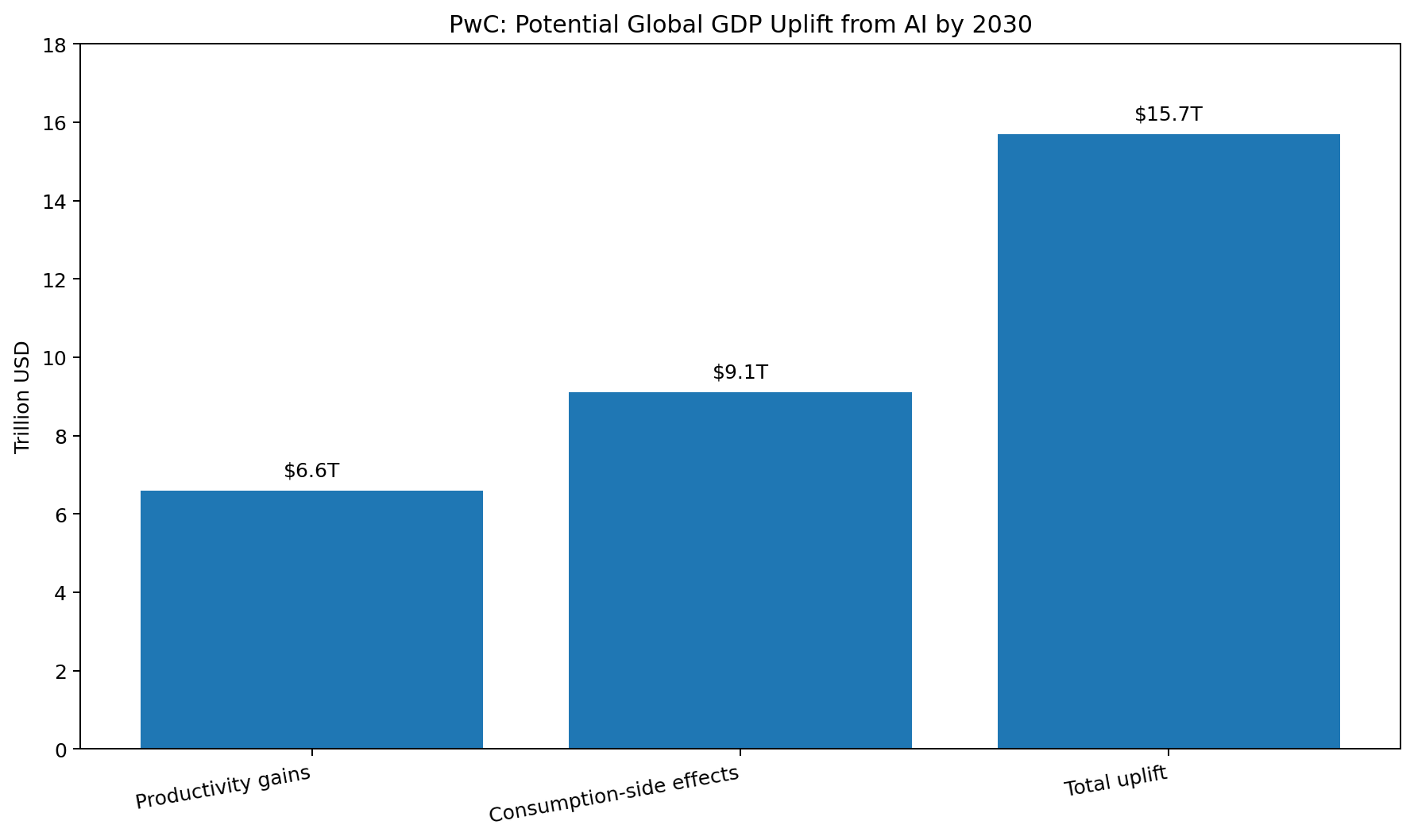

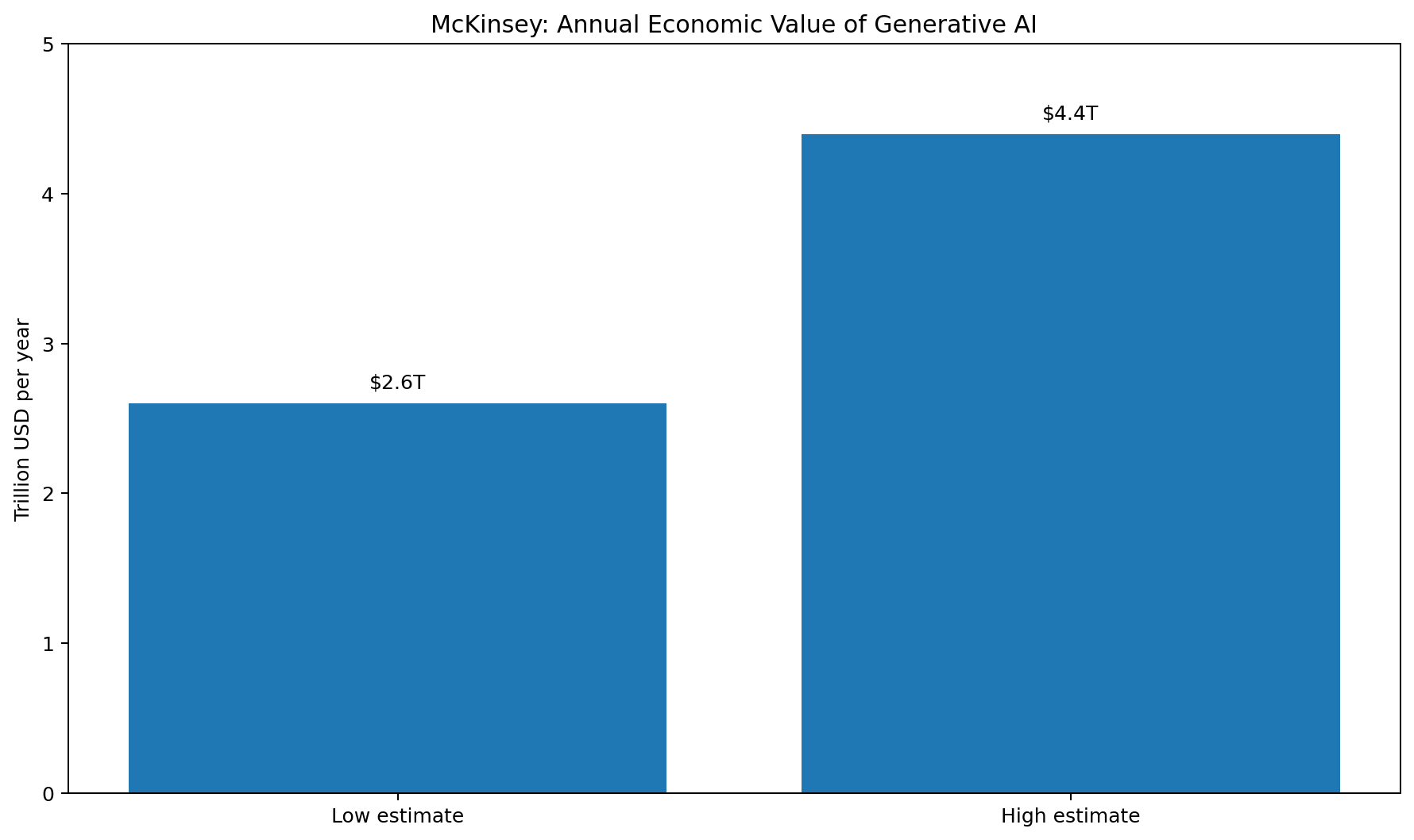

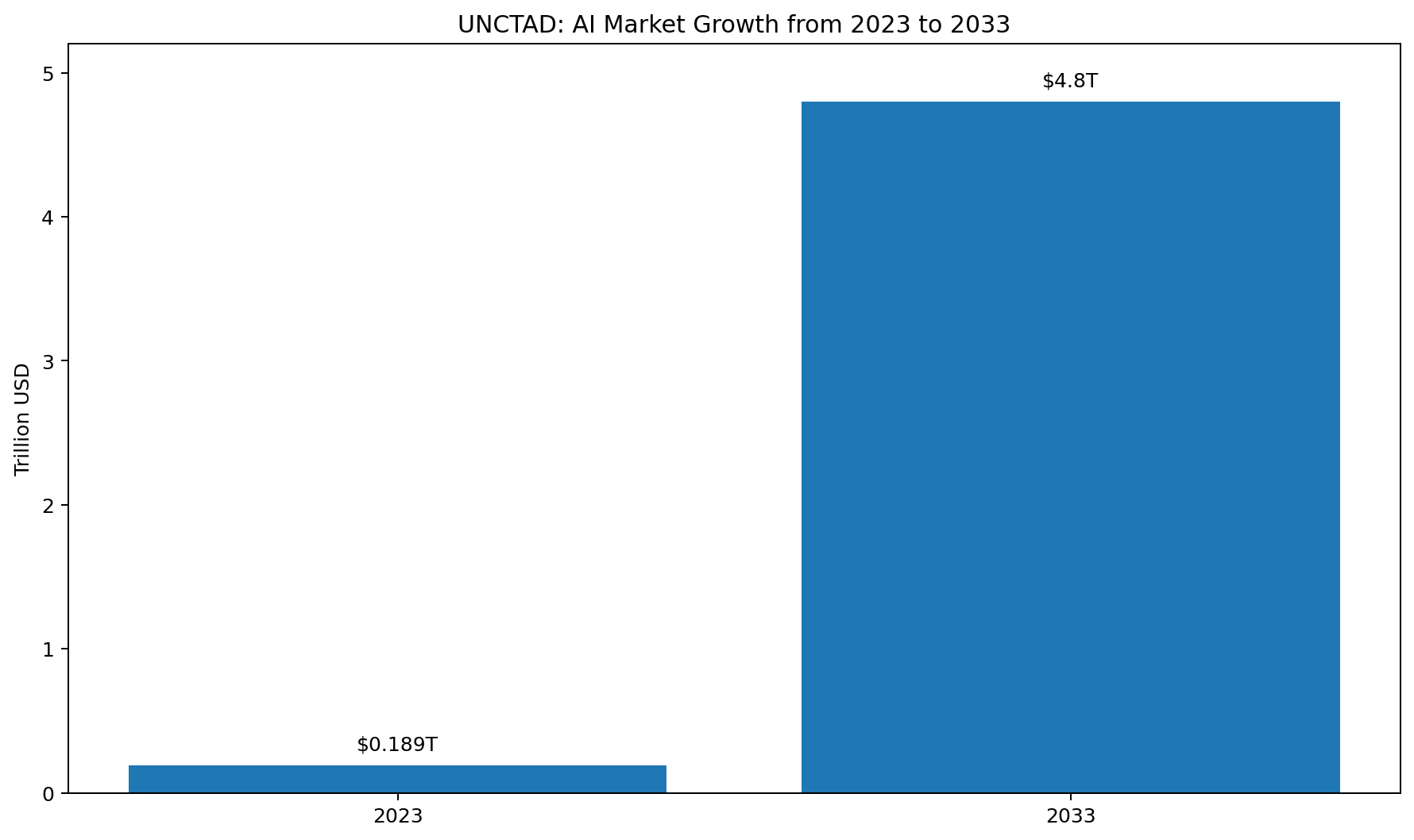

At the top layer the long range forecasts are still massive. PwC’s widely cited estimate says AI could add up to $15.7 trillion to the global economy by 2030 with $6.6 trillion coming from productivity gains and $9.1 trillion from consumption side effects like better products and more personalised demand. McKinsey’s estimate is narrower but still huge! Generative AI alone could add a whopping $2.6 trillion to $4.4 trillion annually across 63 business use cases. UN Trade and Development has projected the AI market could grow from $189 billion in 2023 to $4.8 trillion by 2033. These are the headline numbers that explain why governments, boards and investors are treating AI as a general purpose technology rather than just another software trend.

But this year is where the story gets really interesting because the conversation is no longer only about distant upside. This year’s reports increasingly show AI already affecting investment, productivity, wages, firm performance and consumer value in some hard hitting measurable ways. This makes 2026 feel like the year the economic potential of AI stopped being purely theoretical and actually started showing up in real terms in the data.

AI is already big enough to move macroeconomic numbers

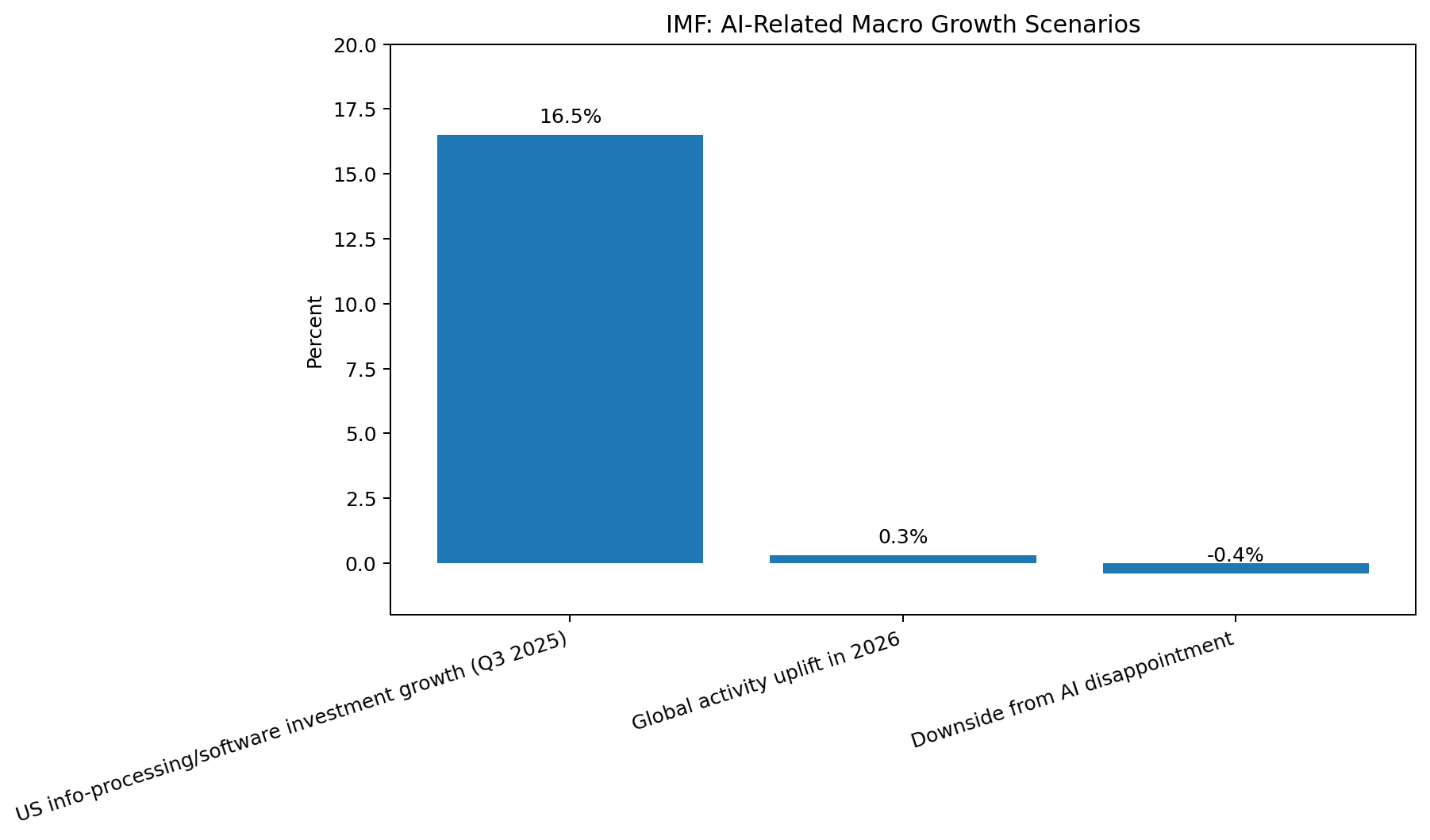

The IMF has become much more explicit in 2026 about AI’s economic significance. In March, Marcello Estevão of the IMF wrote that AI related investment now accounts for a large share of US GDP growth with demand spilling into servers, data centres, software and power infrastructure. He pointed to US investment in information processing equipment and software growing 16.5% year over year in Q3 2025, arguing that without the AI boom, GDP would have been markedly weaker. In its January 2026 outlook and related analysis, the IMF also said AI could raise US and global activity by 0.3% this year relative to baseline if productivity starts coming through more clearly.

This may sound modest but at global scale even a few tenths of a percentage point is a very large number. The same IMF analysis also warned that if AI valuations disappoint and investment falls, global growth could end up 0.4% below baseline in a downside scenario. This tells you something important about AI in 2026: it is now large enough to be an upside engine and a downside macro risk at the same time.

Capital is flooding in at extraordinary speed

One of the clearest signs of AI’s economic potential is simply how much money is chasing it.

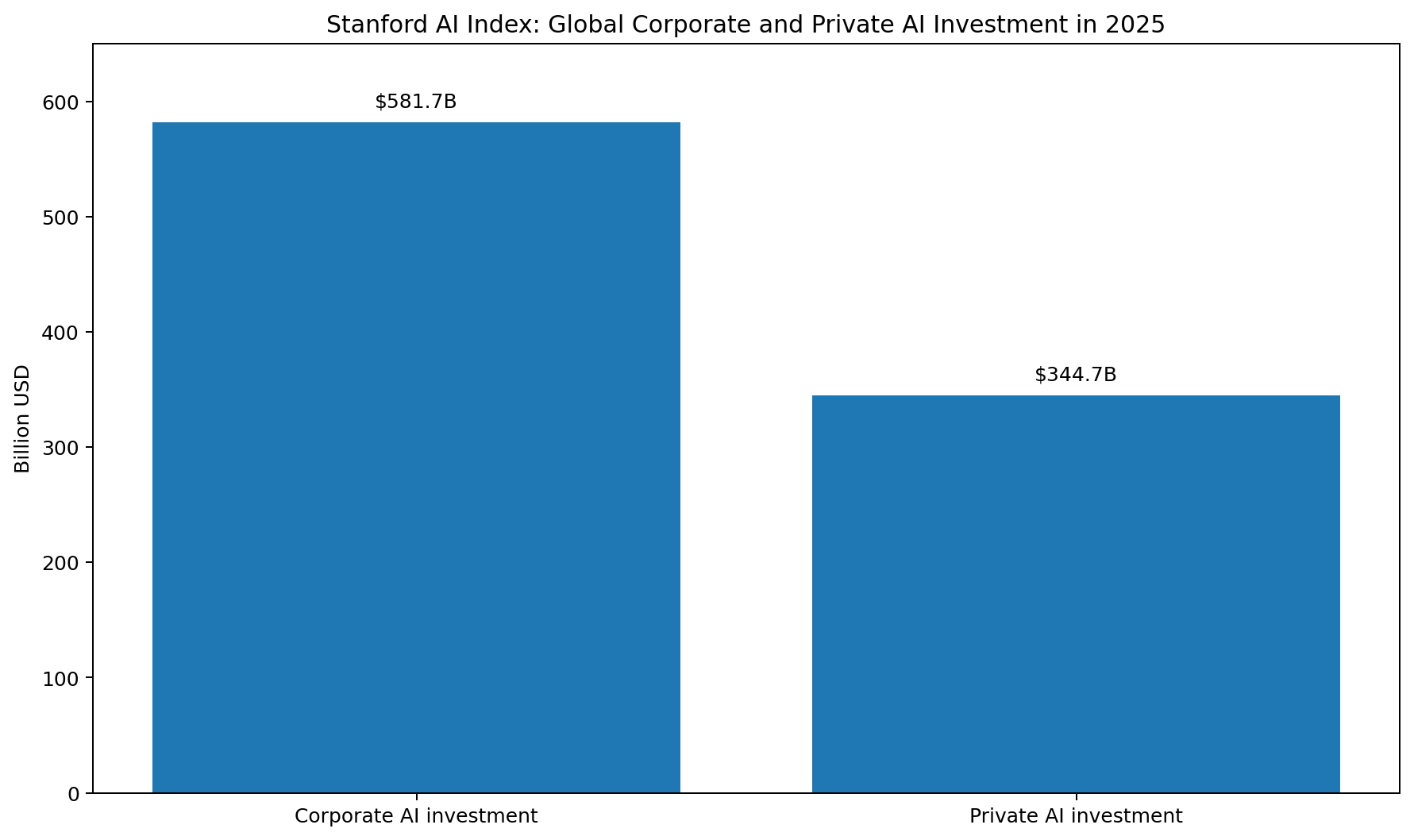

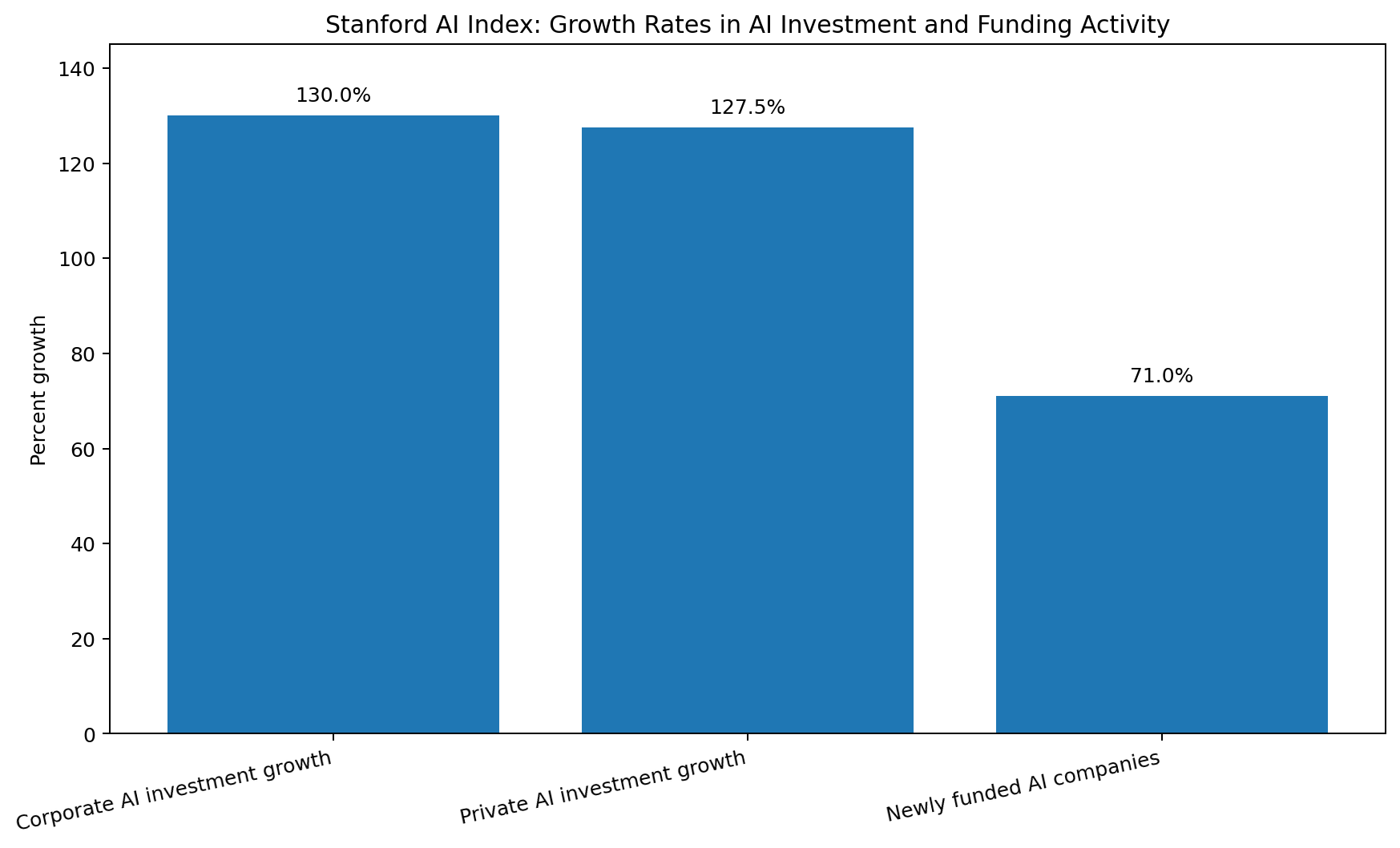

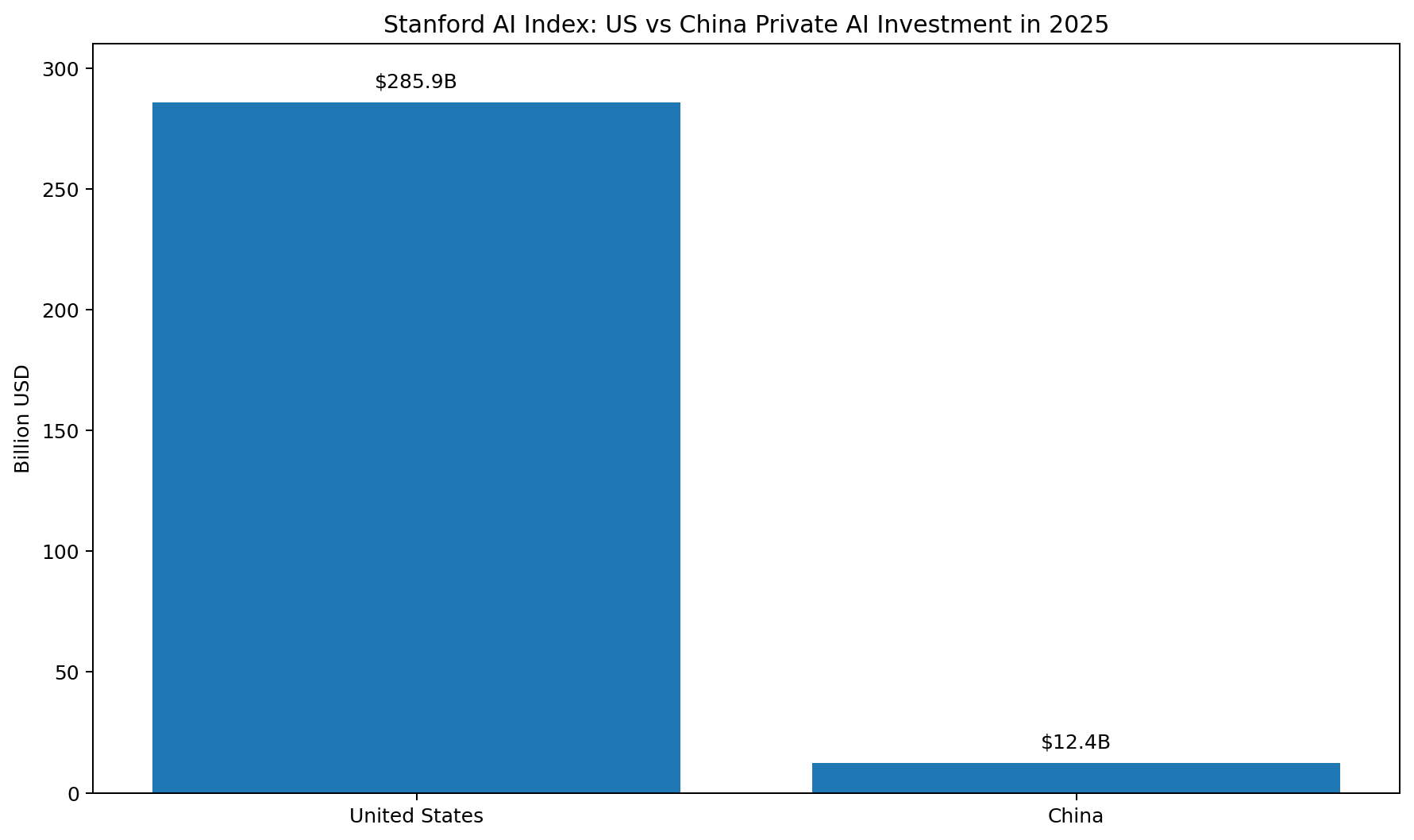

Stanford’s 2026 AI Index says global corporate AI investment hit $581.7 billion in 2025, up 130% from the prior year. Private investment reached $344.7 billion, rising 127.5% year over year. The United States alone accounted for $285.9 billion in private AI investment in 2025, which Stanford says was 23.1 times China’s figure of $12.4 billion. Stanford also notes that newly funded AI companies rose 71%, while billion dollar funding rounds nearly doubled.

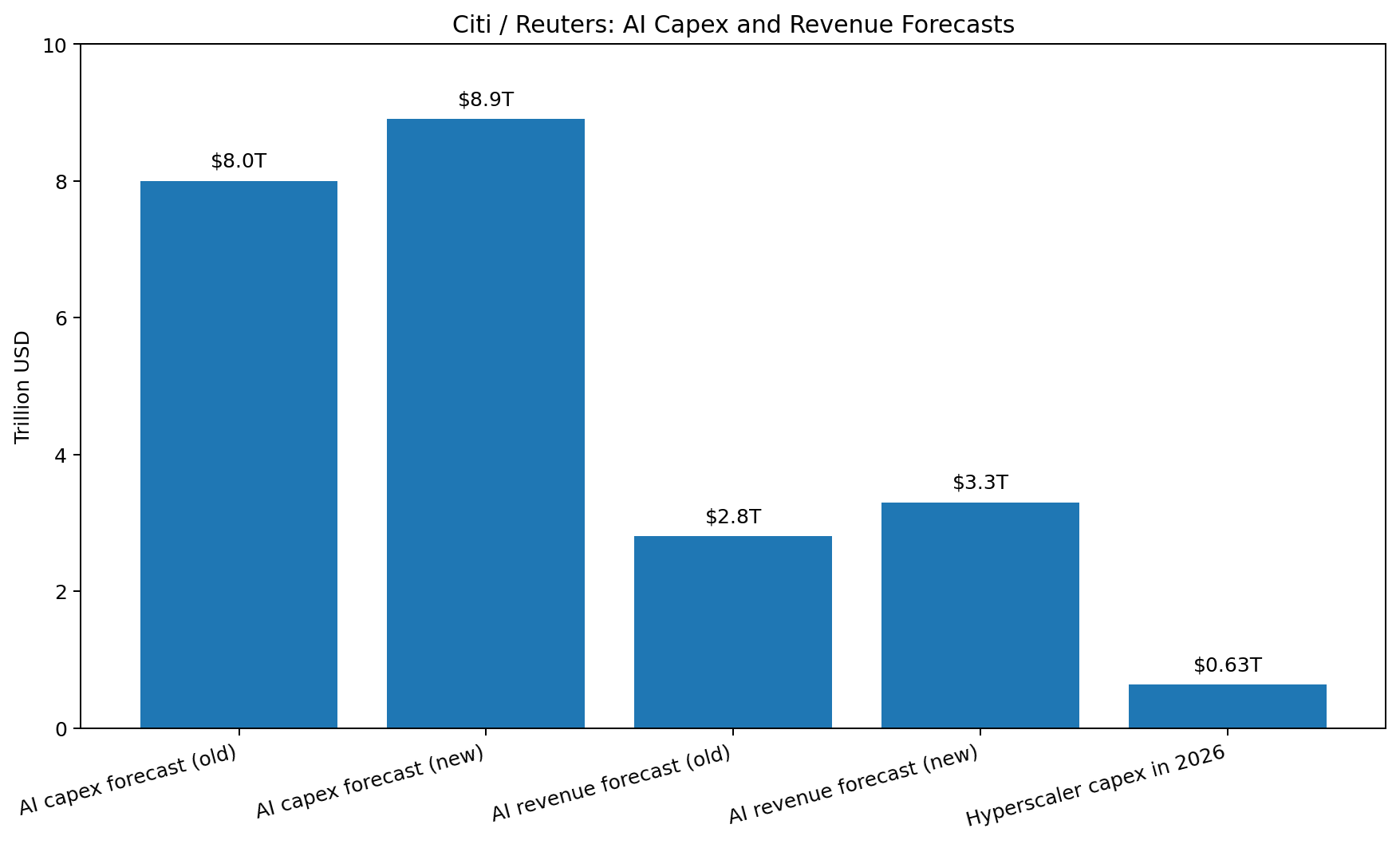

This surge is feeding directly into infrastructure spending. Reuters reported in March 2026 that Citigroup raised its forecast for global AI-related capital expenditure in 2026-2030 to $8.9 trillion, up from $8 trillion previously. Citi also lifted its AI revenue forecast for the same period to $3.3 trillion from $2.8 trillion. And the four big hyperscalers - Amazon, Microsoft, Alphabet and Meta - are expected to spend more than $630 billion in capital expenditure in 2026.

In practical terms, that means AI is no longer only a software story. It is a data centre story, an energy story, a semiconductor story, a networking story and a financing story. That is exactly why so many economists increasingly compare it to electricity or the broader IT buildout rather than to a normal app cycle.

The value is no longer only corporate. Consumers are already capturing it too

One of the most underappreciated parts of AI’s economic potential is the consumer side.

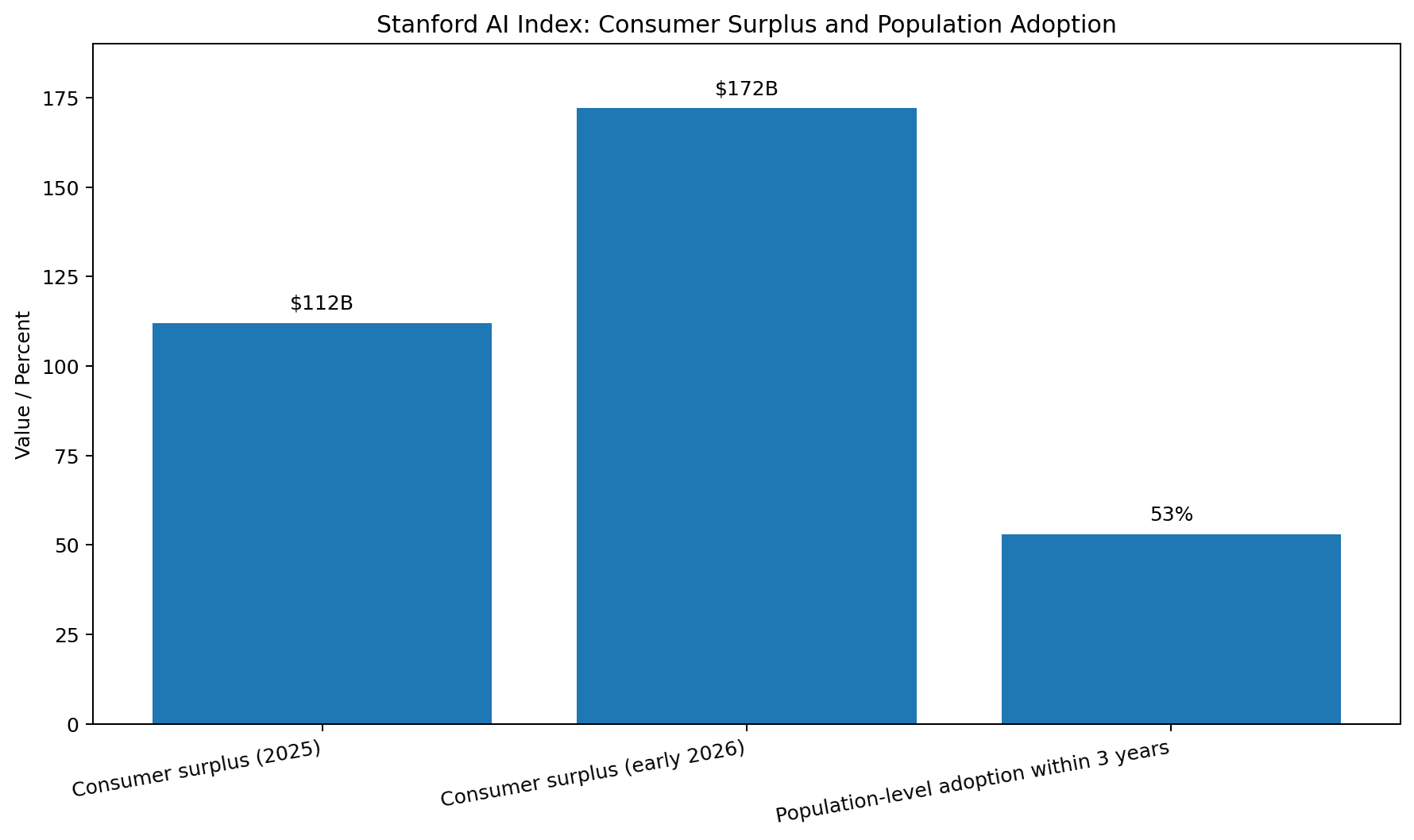

Stanford’s 2026 AI Index estimates that US consumer surplus from generative AI reached $172 billion annually by early 2026, up from $112 billion a year earlier, which is a 54% increase in one year. Stanford also says generative AI reached close to 53% population-level adoption within three years of mass market introduction, faster than the personal computer or the internet.

This matters because economic value does not only show up in company revenue. A lot of it appears as saved time, lower search costs, faster access to information and better outcomes for users even when the tools are free or very cheap. Consumer surplus is one reason AI’s real economic impact can exceed what you see in traditional market size numbers alone.

Productivity is the biggest near term prize

The strongest economic case for AI in 2026 is still productivity.

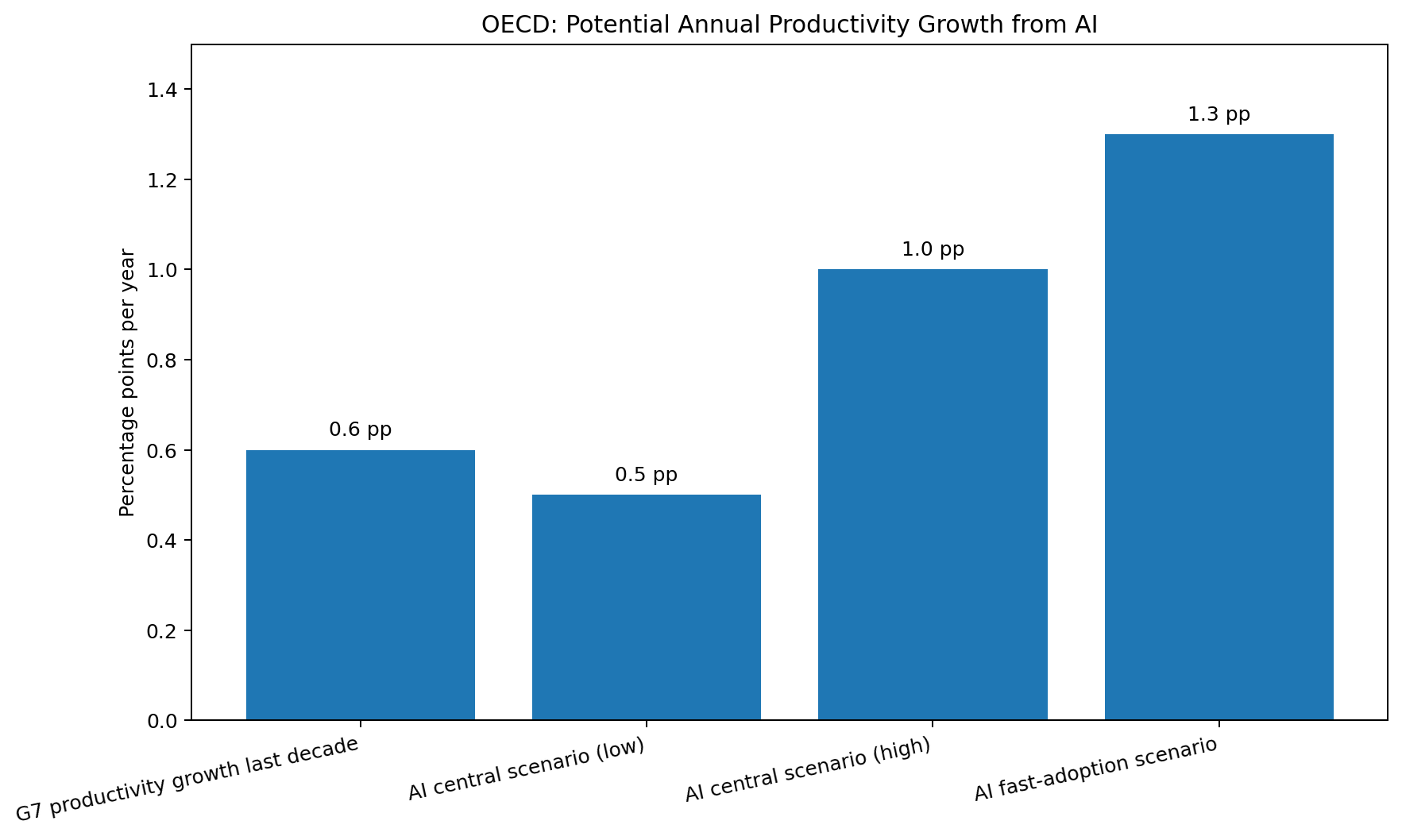

OECD analysis published in April 2026 estimates that AI could raise annual labour productivity growth across G7 economies by 0.5 to 1 percentage point over the next decade in its central scenario. OECD also notes that average annual labour productivity growth across the G7 was only 0.6% over the last ten years, which means the AI dividend could be close to doubling recent productivity growth rates. In a faster-adoption scenario, OECD says the gain could reach 1.3 percentage points a year.

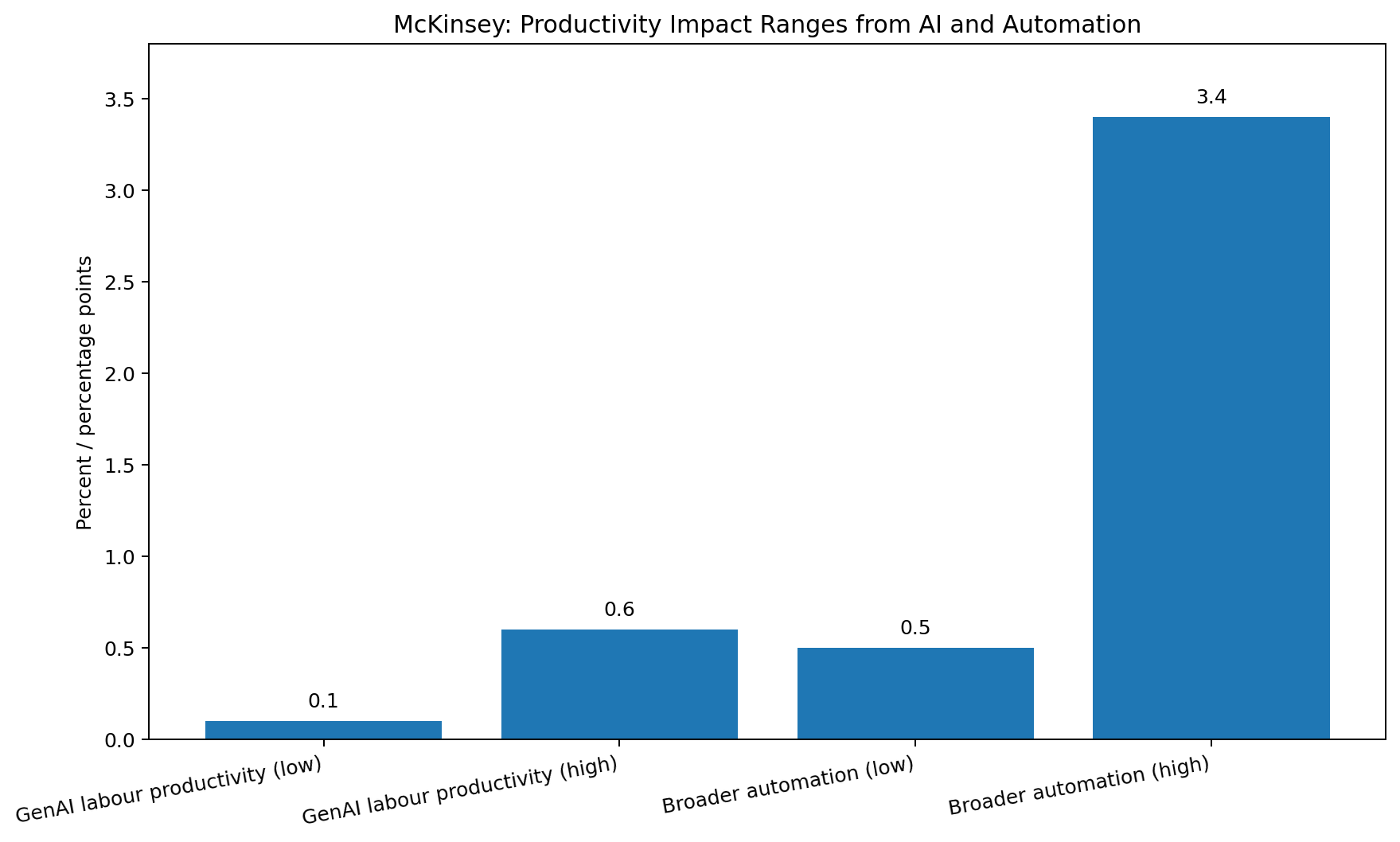

McKinsey’s longer range estimate is also still influential here. It says generative AI could enable labour productivity growth of 0.1 to 0.6 percentage points annually through 2040 and that broader automation technologies could deliver a global annual productivity boost of 0.5 to 3.4% depending on adoption and redeployment.

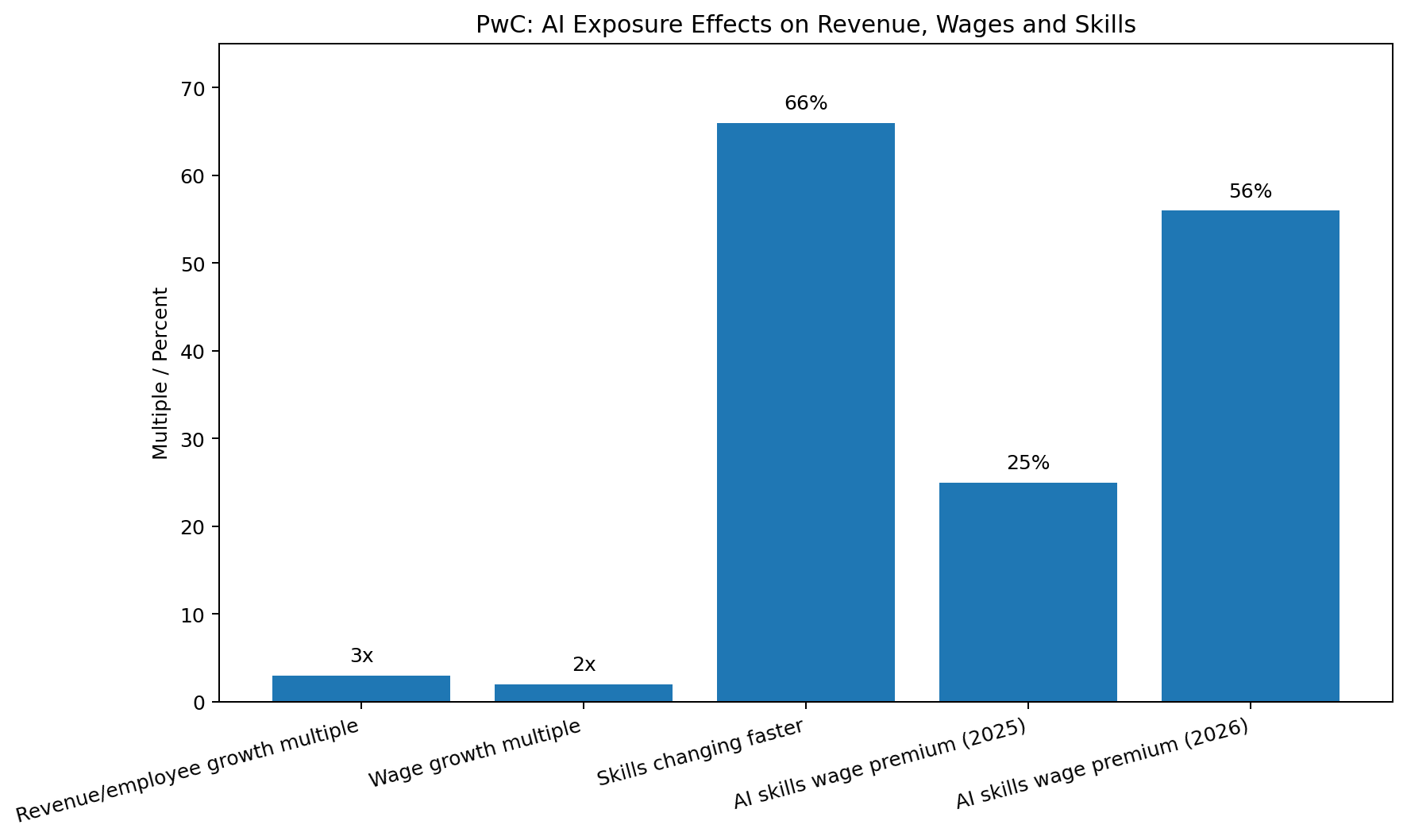

The labour market data is starting to line up with this story. PwC’s AI Jobs Barometer says industries more exposed to AI have seen 3x higher growth in revenue per employee since 2022. It also says wages are rising 2x faster in the most AI exposed industries, skills are changing 66% faster in AI exposed jobs than in others and workers with AI skills command a 56% wage premium, up from 25% a year earlier.

These figures do not prove AI has solved the productivity puzzle for the whole economy yet. But they do show that AI is already creating measurable economic value inside firms and labour markets, especially where adoption is deeper and more systematic.

The gains are real but they are not spreading evenly

This is where the 2026 evidence gets especially important.

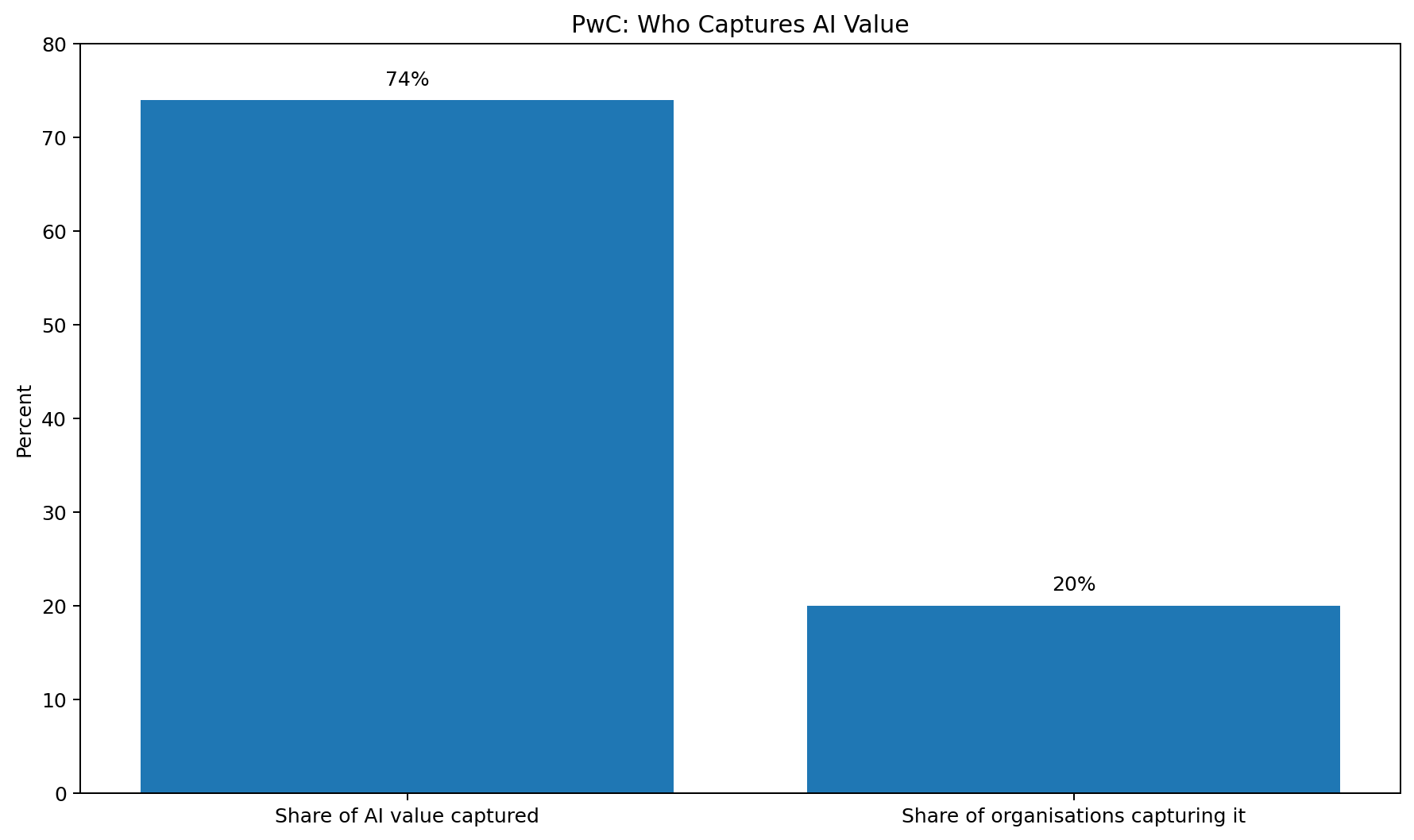

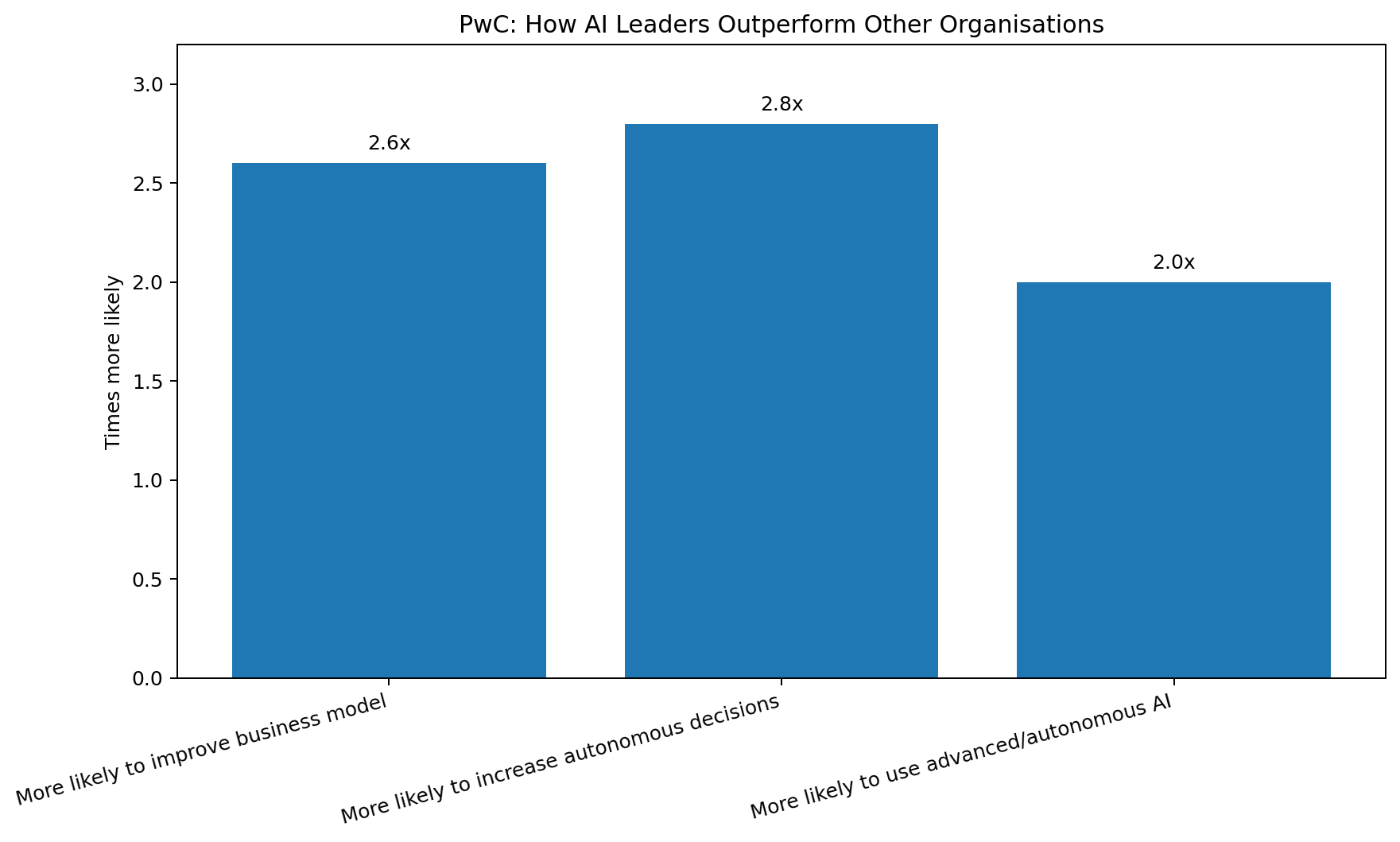

PwC’s April 2026 AI Performance Study found that 74% of AI’s economic value is being captured by just 20% of organisations. This is a huge concentration of gains. The leaders are not merely using more AI tools; PwC says they are 2.6 times as likely to report that AI improves their ability to reinvent their business model, 2.8 times as likely to increase decisions made without human intervention and nearly twice as likely to use AI in advanced or autonomous ways.

This suggests the economic potential of AI will not be unlocked evenly across the market. It will likely favour companies that combine AI with workflow redesign, governance, data quality and faster decision making. In other words, AI may widen performance gaps before it narrows them.

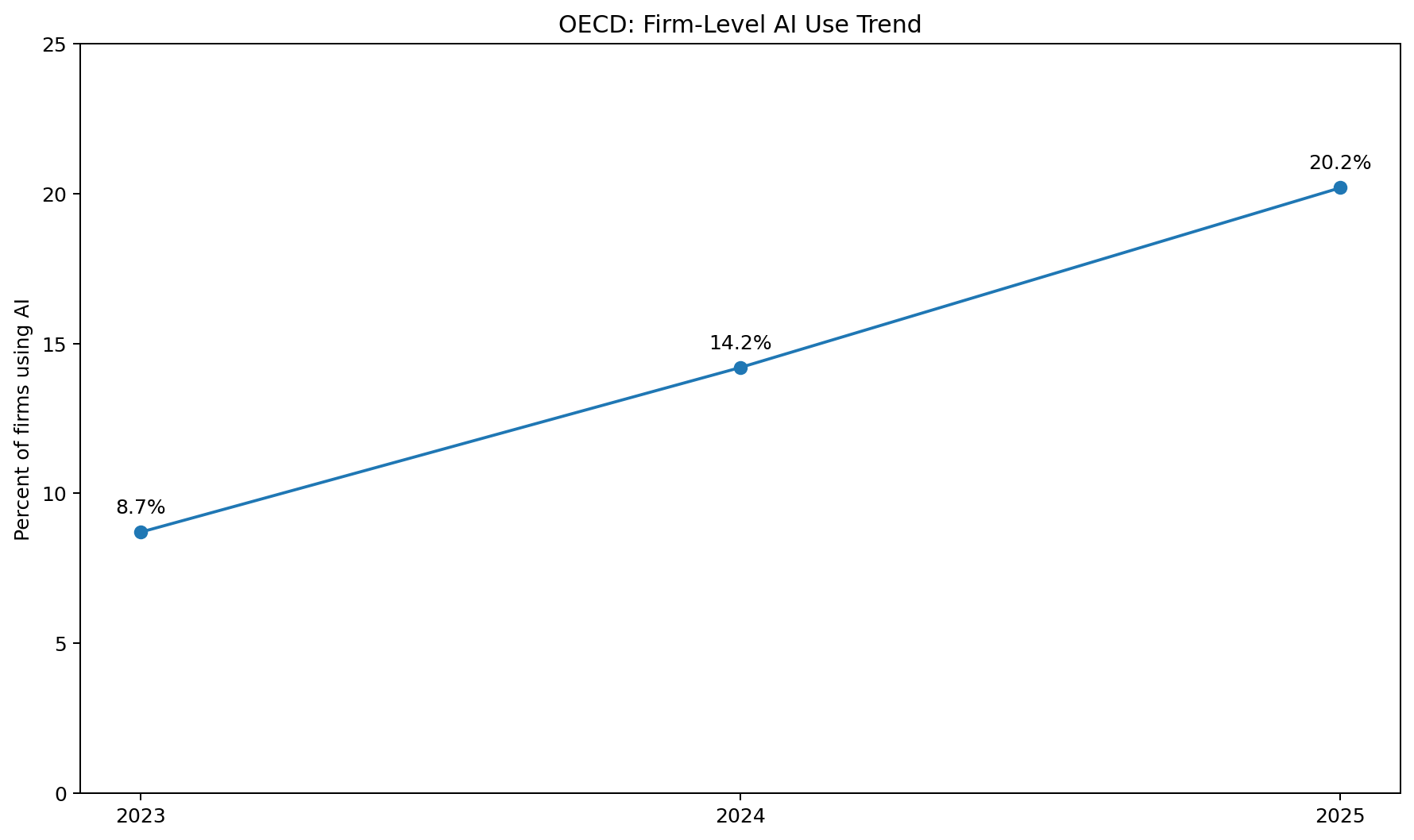

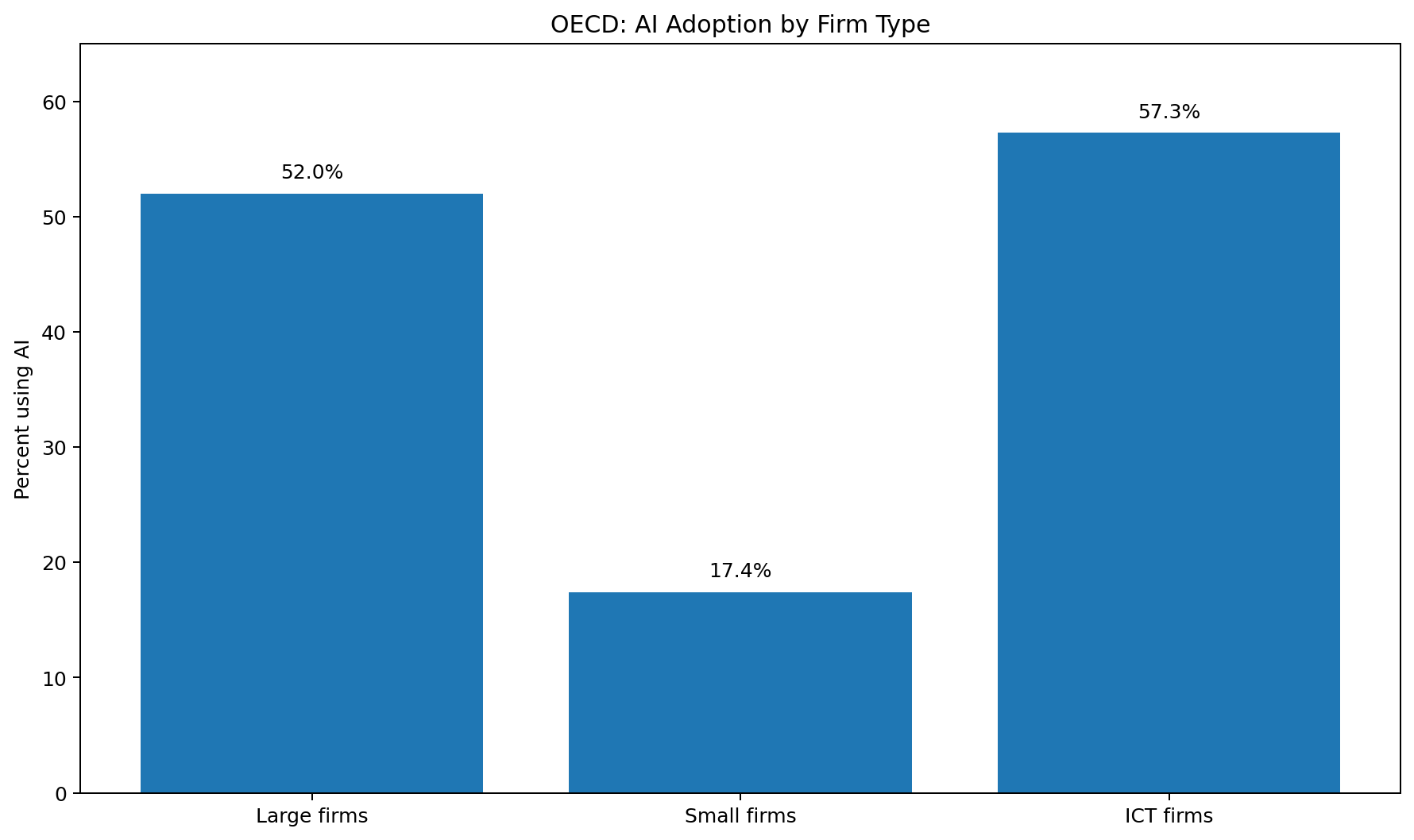

The same pattern appears internationally. OECD data released in January 2026 says firm level AI use across OECD countries rose to 20.2% in 2025 up from 14.2% in 2024 and 8.7% in 2023. But adoption is highly uneven by firm size! 52.0% of large firms use AI versus only 17.4% of small firms. Industry gaps are also wide... 57.3% of ICT firms use AI compared with much lower levels elsewhere, even though lagging sectors like accommodation, food services and construction are now growing faster from a lower base.

This unevenness matters economically. If AI stays concentrated in large firms, leading sectors and rich countries then the gains to aggregate GDP may come through slower than the biggest forecasts. OECD explicitly says wider productivity gains will depend on diffusion, skills and competitive market structures, especially for SMEs.

Market size is not the same as economic impact but both are exploding

There is also a difference between the AI market itself and the broader value AI creates across the economy.

UNCTAD’s estimate of a $4.8 trillion AI market by 2033 is about the size of the AI sector and related commercial value. PwC’s $15.7 trillion figure is about total GDP uplift. McKinsey’s $2.6 trillion to $4.4 trillion annually is about potential business value from generative AI use cases. Citi’s $3.3 trillion forecast for AI revenue in 2026-2030 is closer to sector level sales. Stanford’s $172 billion US consumer surplus estimate captures value not fully reflected in company revenues.

Put together, these numbers all point in the same direction: AI’s economic potential is not one thing. It is a stack of effects that includes sector revenue, capital formation, productivity growth, wage effects, consumer surplus and eventually GDP expansion. The reason estimates vary so much is that they are measuring different layers of the same phenomenon.

The biggest question in 2026 is no longer 'Is AI valuable?'

It is 'Who captures the value, how fast and at what cost?'

This is the real economic debate now.

On the upside the data supports the idea that AI can raise productivity, speed up growth and generate very large gains in both producer and consumer value. On the downside, the IMF, OECD and others are warning about concentration, skills bottlenecks and the risk that these expectations will outrun real productivity.

So the smartest way to describe the economic potential of AI in 2026 is this:

AI still has a trillion dollar upside. This part has not changed.

What has changed is that we now have stronger evidence that some of the gains are already real. Investment is surging. Infrastructure is scaling. Consumer surplus is measurable. Productivity signals are appearing. Wages are moving. Firm performance gaps are widening. The long term promise is still uncertain in size and timing but the economic engine is already running.

Sources

https://www.imf.org/en/publications/weo/issues/2026/01/19/world-economic-outlook-update-january-2026

https://hai.stanford.edu/ai-index/2026-ai-index-report/economy

https://hai.stanford.edu/news/inside-the-ai-index-12-takeaways-from-the-2026-report

https://hai.stanford.edu/assets/files/ai_index_report_2026_chapter_4_economy.pdf

https://www.pwc.com/gx/en/news-room/press-releases/2026/pwc-2026-ai-performance-study.html

https://www.pwc.com/gx/en/services/ai/ai-jobs-barometer.html