Ecommerce statistics in 2026

Ecommerce in 2026 is not just 'still growing'.

It is getting bigger, more mobile, more payment driven and more uneven at the same time. The latest numbers show a market that is still expanding globally but where execution matters more than ever. Online retail is taking a larger share of total commerce, mobile is becoming the default shopping channel, digital wallets are hardening into the global payments baseline and regions like Latin America are growing faster than the global average. On the other hand, weak checkout experiences, poor delivery and opaque pricing are still killing conversions at scale!

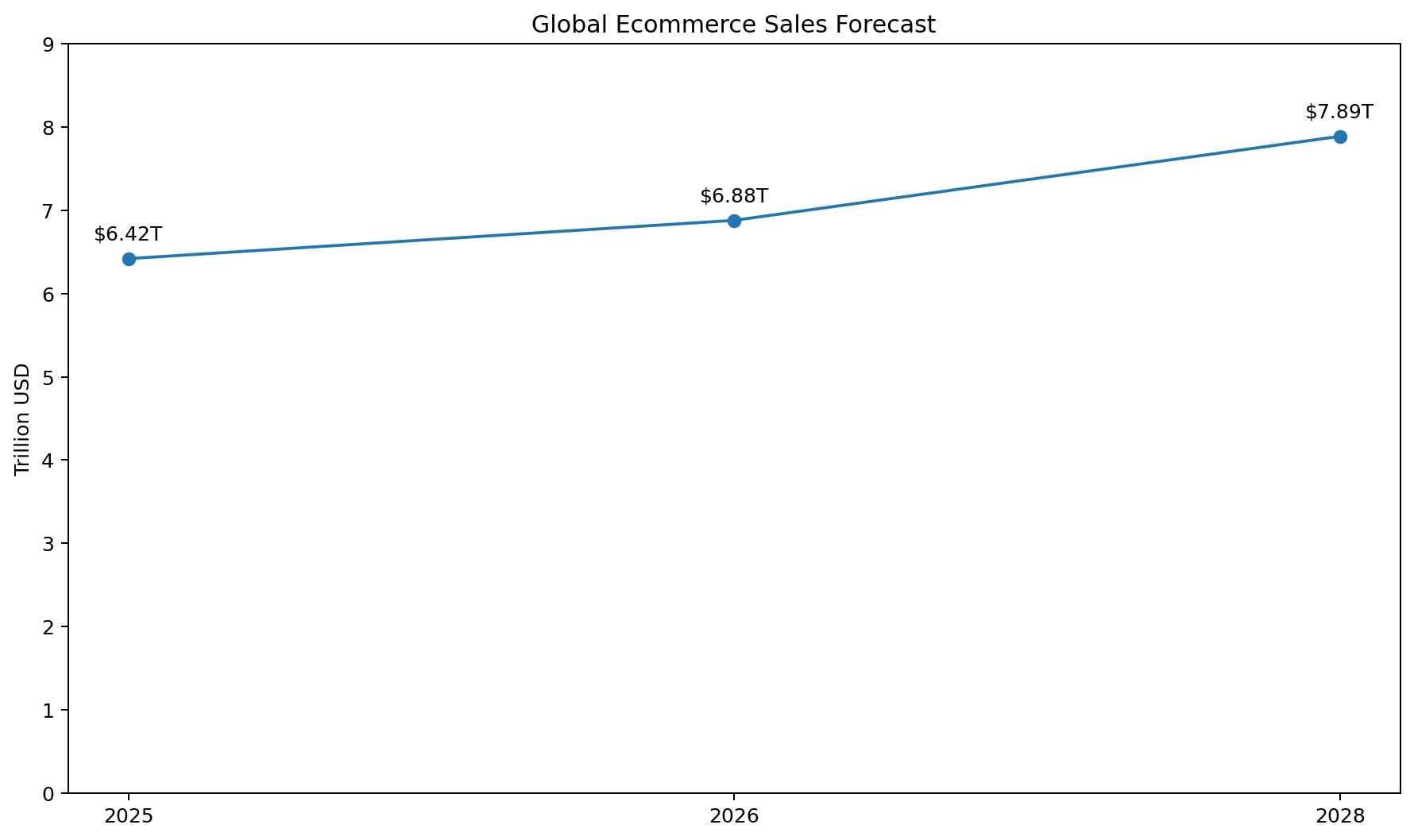

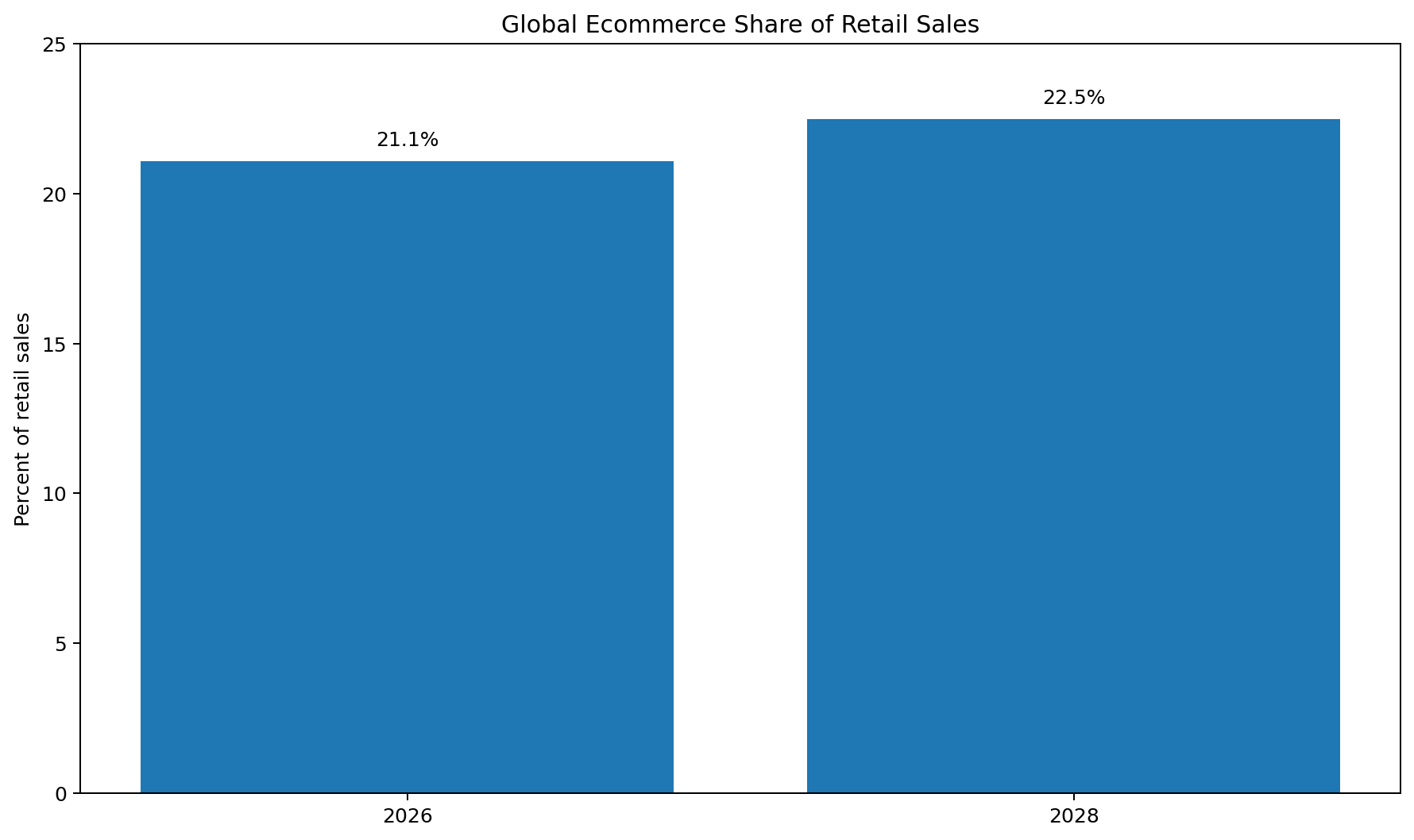

The big headline is simple: global ecommerce is now forecast to reach $6.88 trillion in 2026, up from $6.42 trillion in 2025 which is a 7.2% year on year increase. Ecommerce is also expected to make up 21.1% of total retail sales in 2026. By 2028, that figure is projected to reach 22.5% with global ecommerce sales rising to $7.89 trillion.

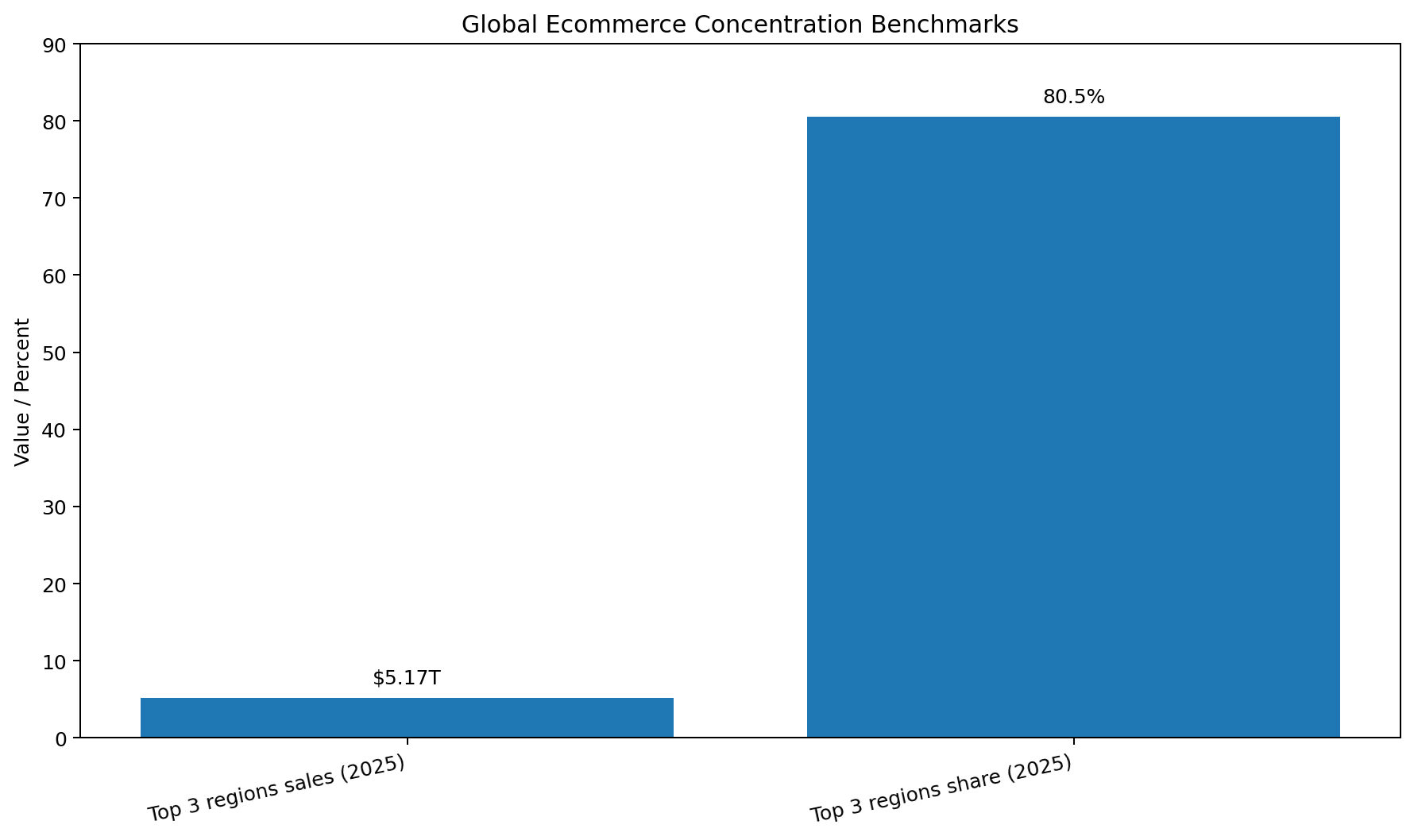

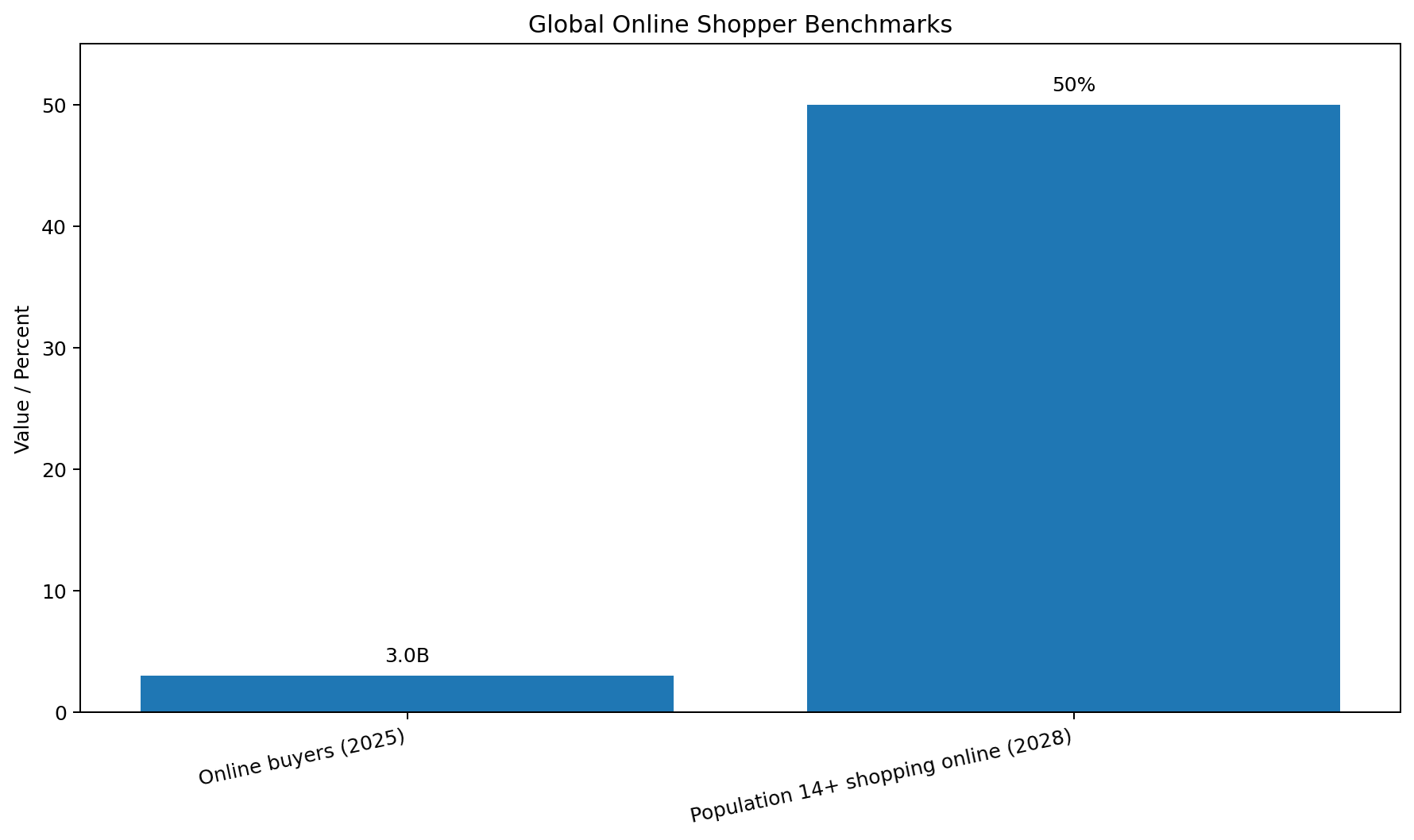

That means ecommerce is no longer just a growth channel. It is now a core share taker from offline retail. Shopify’s summary of EMARKETER forecasts also says that in 2025 the three biggest contributors to global ecommerce were China, the United States and Western Europe, which together accounted for more than $5.17 trillion in sales and 80.5% of global ecommerce sales. It also notes that more than 3 billion people are expected to buy online in 2025 and that by 2028 50% of the global population aged 14 and older will be online shoppers.

Ecommerce is still growing, but not all growth looks the same

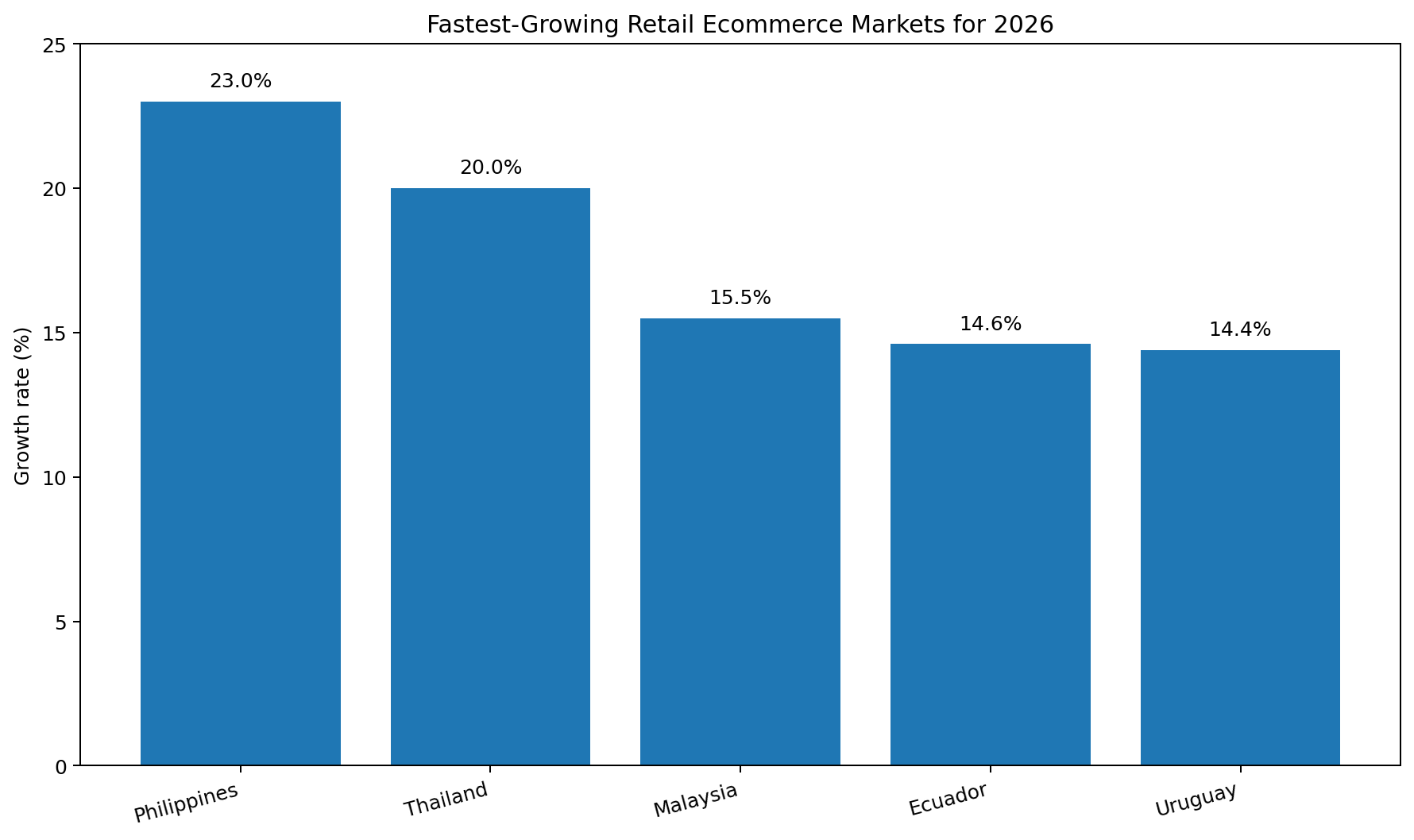

A useful reality check is that ecommerce growth is now being driven by both scale and geography. Large mature markets still dominate total sales but emerging markets are helping keep overall growth rates healthy. Shopify’s 2026 report says the Philippines is expected to grow retail ecommerce sales by 23% with Thailand at 20%, Malaysia at 15.5%, Ecuador at 14.6% and Uruguay at 14.4%. This tells you the next wave of ecommerce expansion is not just about the US and China getting bigger. It is also about newer digital markets accelerating faster!

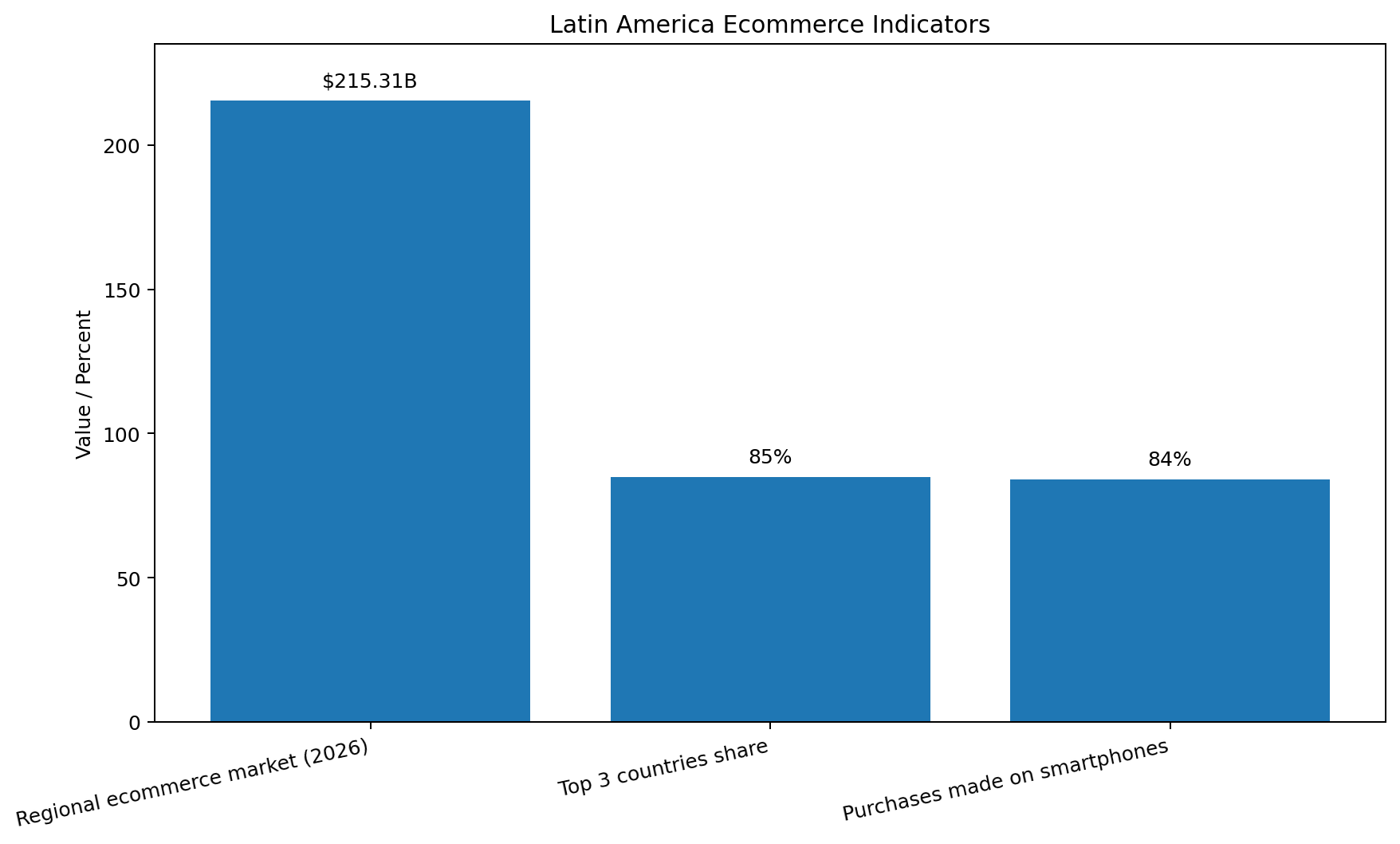

Latin America is one of the clearest examples. Reuters reported in January 2026 that ecommerce in Latin America is projected to reach $215.31 billion in 2026, growing 1.5 times faster than the global average. The region is highly concentrated with Argentina, Brazil and Mexico accounting for nearly 85% of regional online sales in 2025. It is also strongly mobile first with 84% of purchases made on smartphones.

This mobile first trend matters because it changes everything from site design to payments to merchandising. It also makes weak experiences even more dangerous. Reuters noted that nearly half of Latin American consumers would stop buying from a platform after a bad experience while three quarters said transparent prices and policies were very important. Fewer than one third rated personalisation as very important. In other words, many retailers are still over investing in recommendation layers while under investing in reliability, delivery and returns.

The US ecommerce market is still huge and still taking share

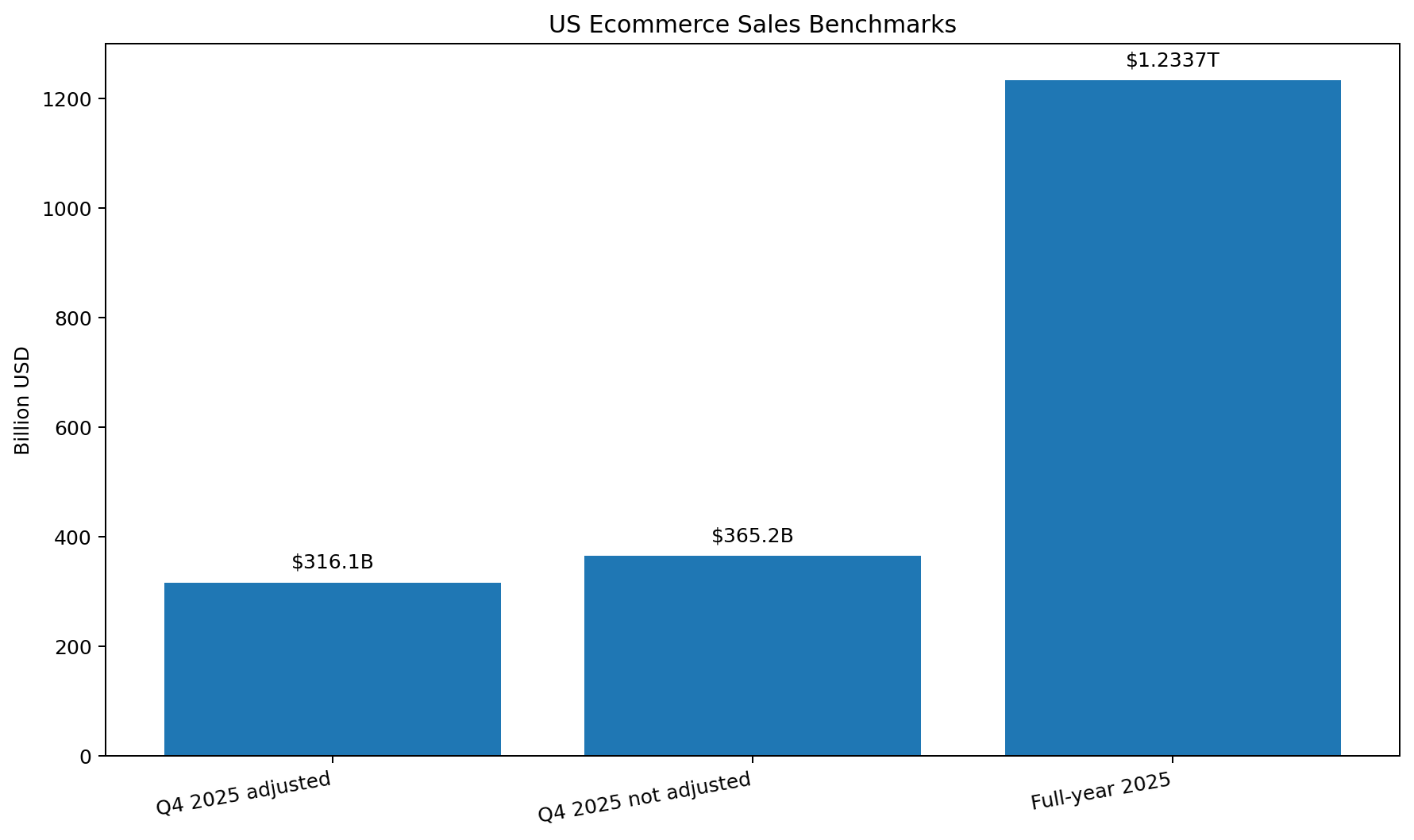

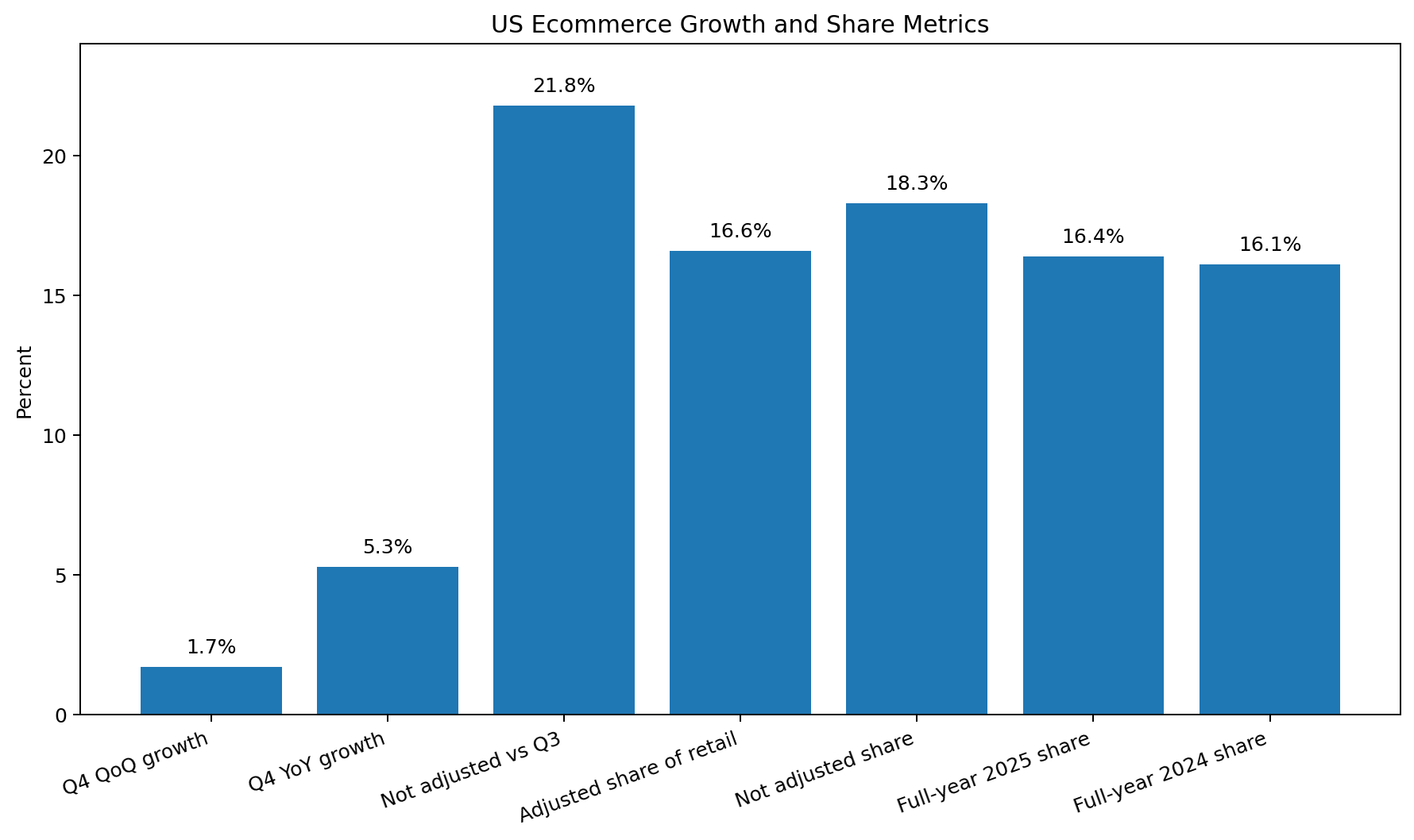

The newest official US government data shows ecommerce continuing to grow faster than total retail. The US Census Bureau reported that adjusted US retail ecommerce sales were $316.1 billion in Q4 2025, up 1.7% quarter on quarter and 5.3% year on year. Ecommerce represented 16.6% of total US retail sales in that quarter on an adjusted basis. On a not adjusted basis, Q4 2025 US retail ecommerce sales were $365.2 billion, up 21.8% from Q3 2025 and ecommerce accounted for 18.3% of total sales. For full year 2025, the Census Bureau estimated US ecommerce sales at $1.2337 trillion, up 5.4% from 2024 with ecommerce accounting for 16.4% of total retail sales, versus 16.1% in 2024. Those figures were released in March 2026, so they are some of the freshest official US ecommerce benchmarks available right now.

This is important because it shows ecommerce is not plateauing. Growth is no longer explosive in the way it was during the pandemic era but it is still outpacing overall retail and steadily taking share.

Mobile is no longer a trend. It is the default

If there is one theme running through almost every recent ecommerce dataset, it is that mobile now dominates consumer behaviour.

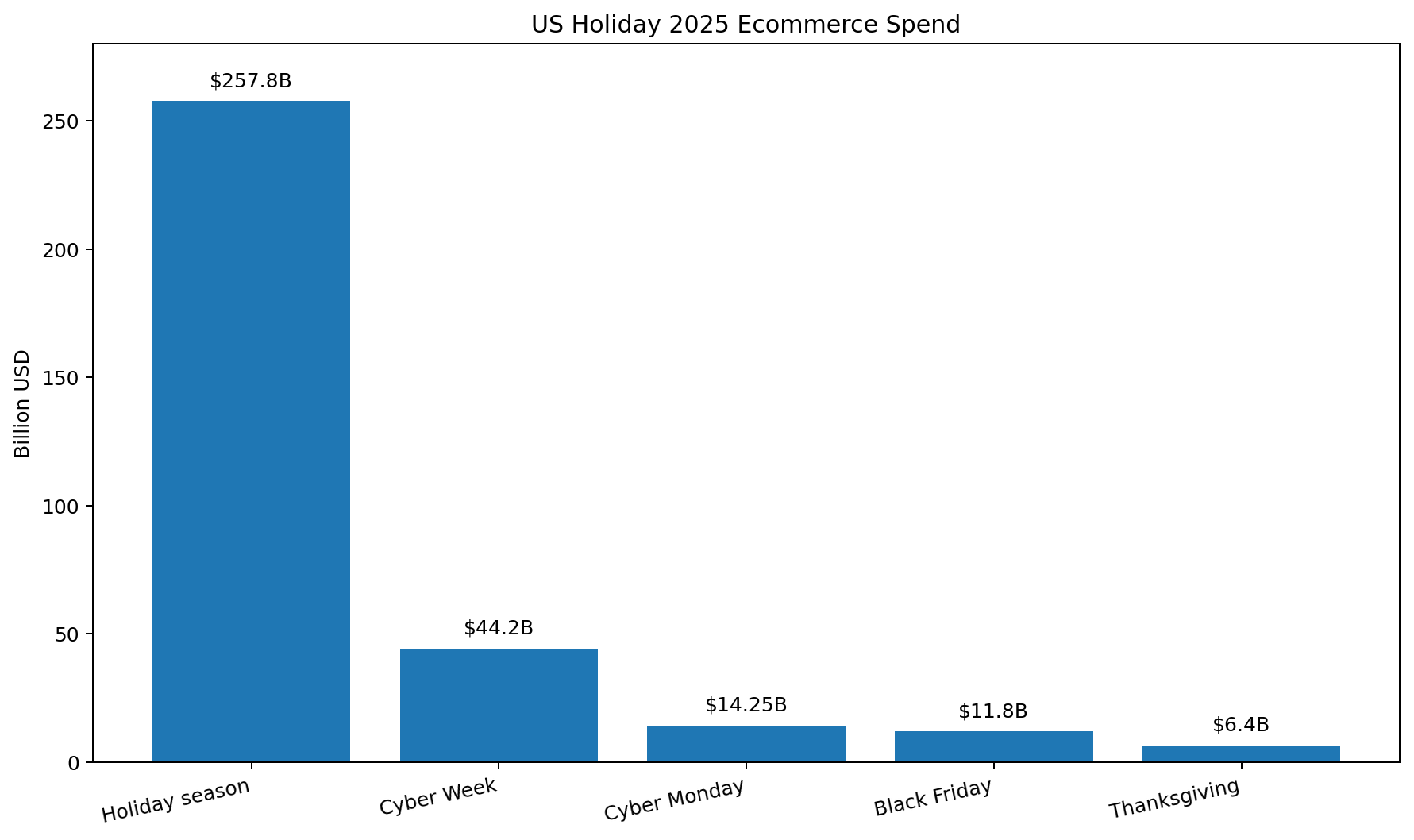

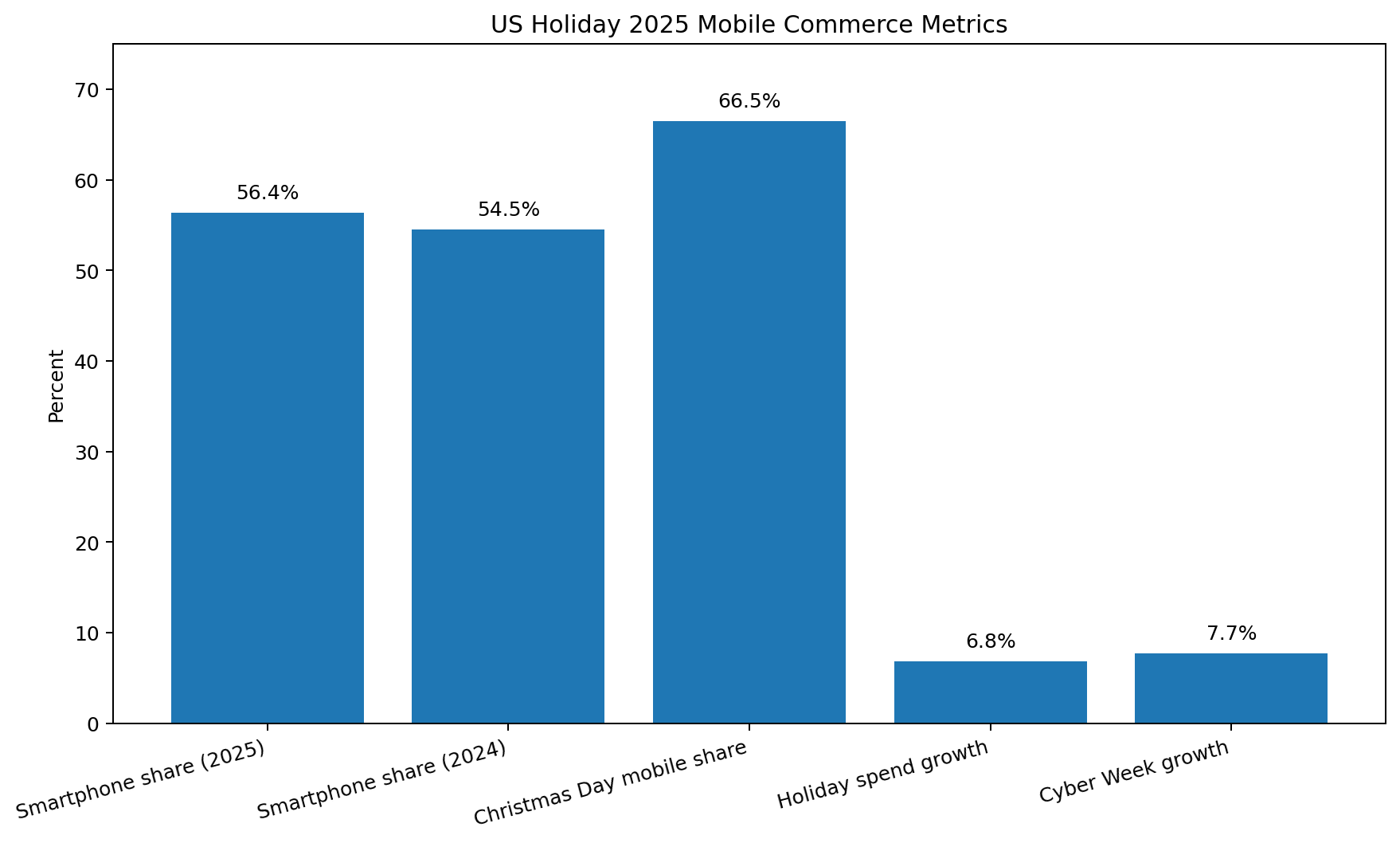

Adobe’s US holiday 2025 data, released in January 2026, found that consumers spent $257.8 billion online from 1 November to 31 December 2025, up 6.8% year on year. During this period, 56.4% of online transactions took place through smartphones, up from 54.5% in 2024. On Christmas Day, mobile drove 66.5% of online sales. Adobe also found that Cyber Week generated $44.2 billion in online spend, up 7.7% year on year with Cyber Monday reaching $14.25 billion, Black Friday $11.8 billion and Thanksgiving Day $6.4 billion.

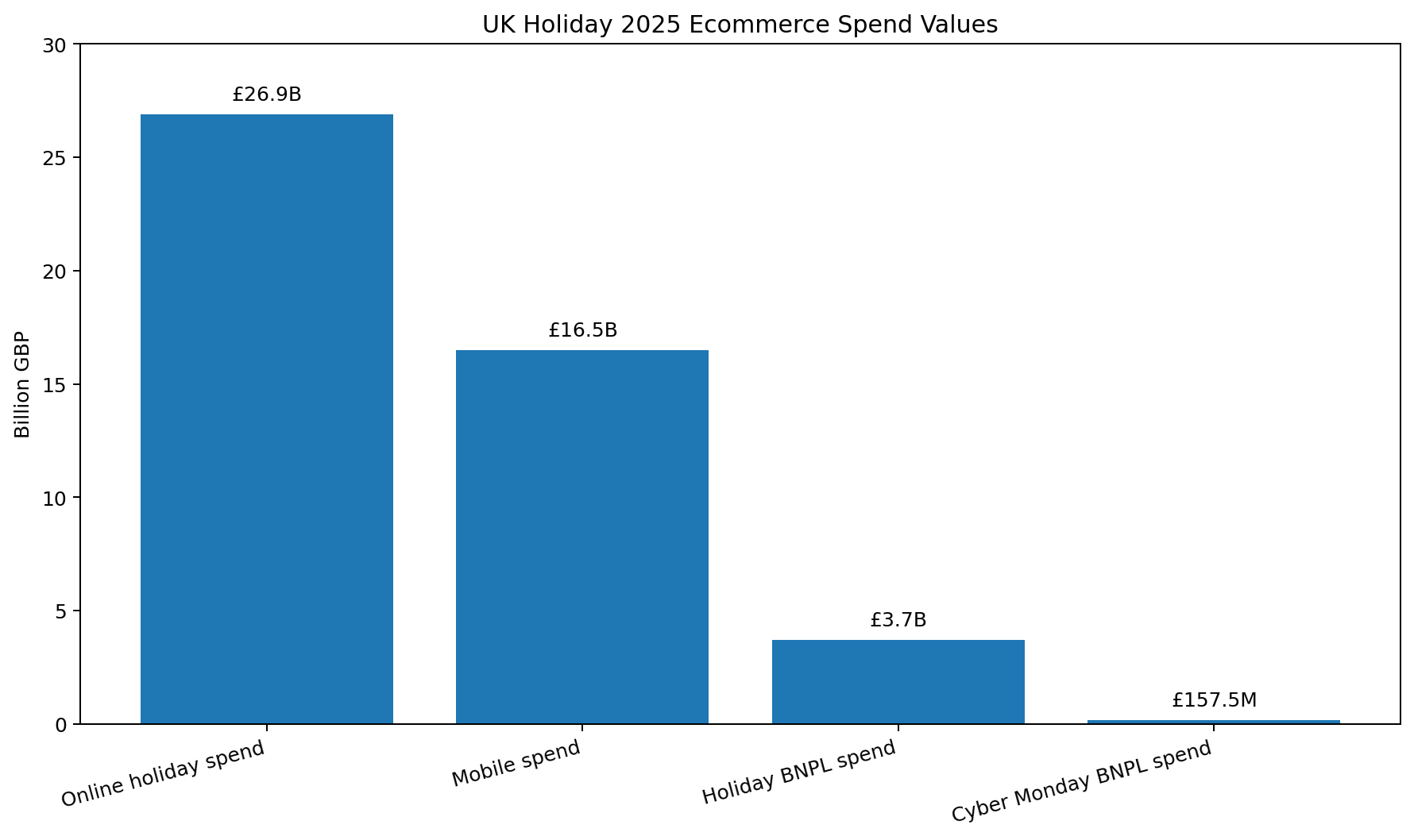

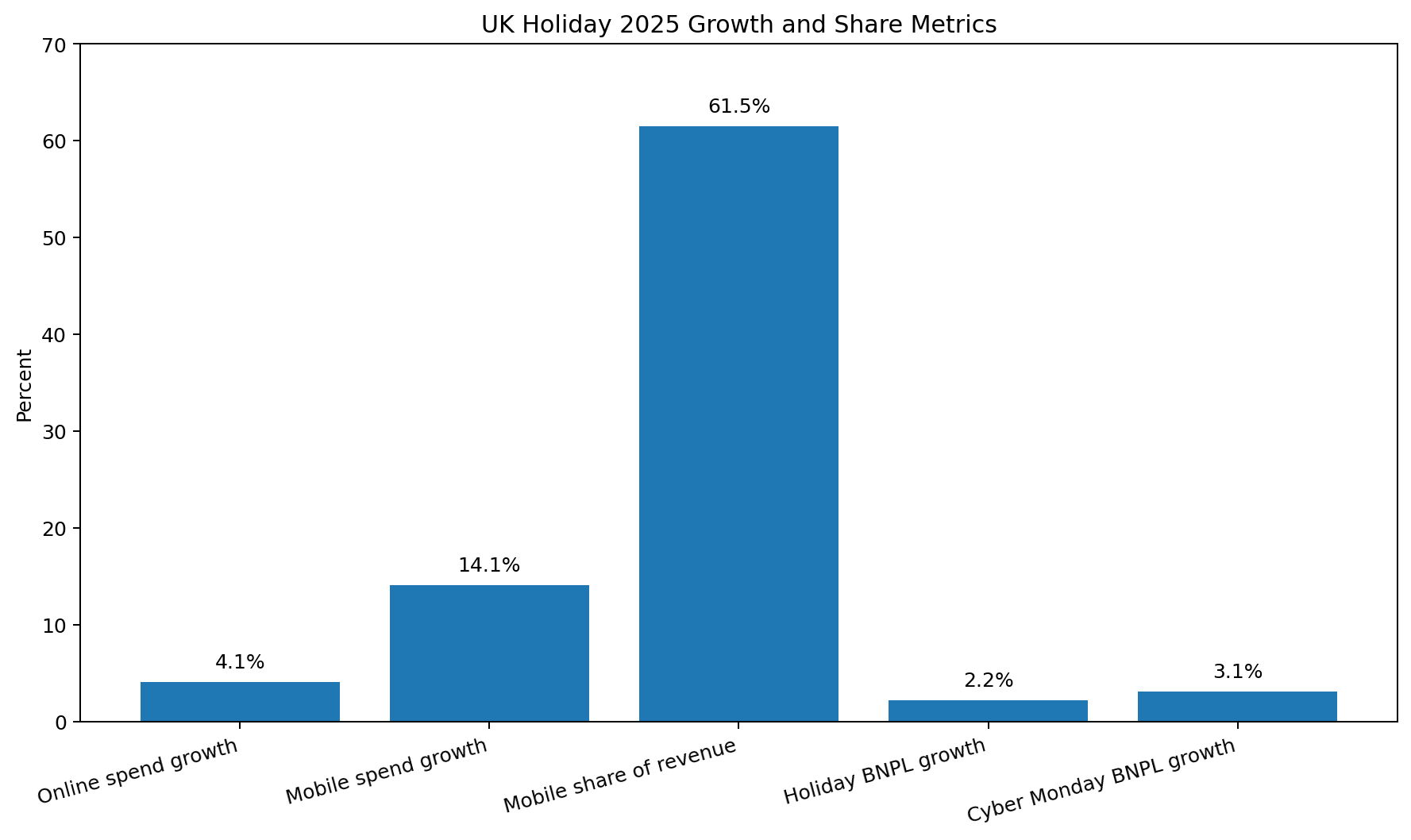

The UK showed the same direction. Adobe’s UK holiday figures, also published in January 2026, show that UK consumers spent a record £26.9 billion online during the 2025 holiday season, up 4.1% year on year. Mobile spend reached £16.5 billion, up 14.1% year on year and mobile’s share of holiday online revenue hit 61.5%.

This is why mobile ecommerce can no longer be treated as a responsive design checkbox. In practice, it is the main storefront.

Payments are becoming one of the biggest competitive edges

The latest 2026 payments data makes that even clearer.

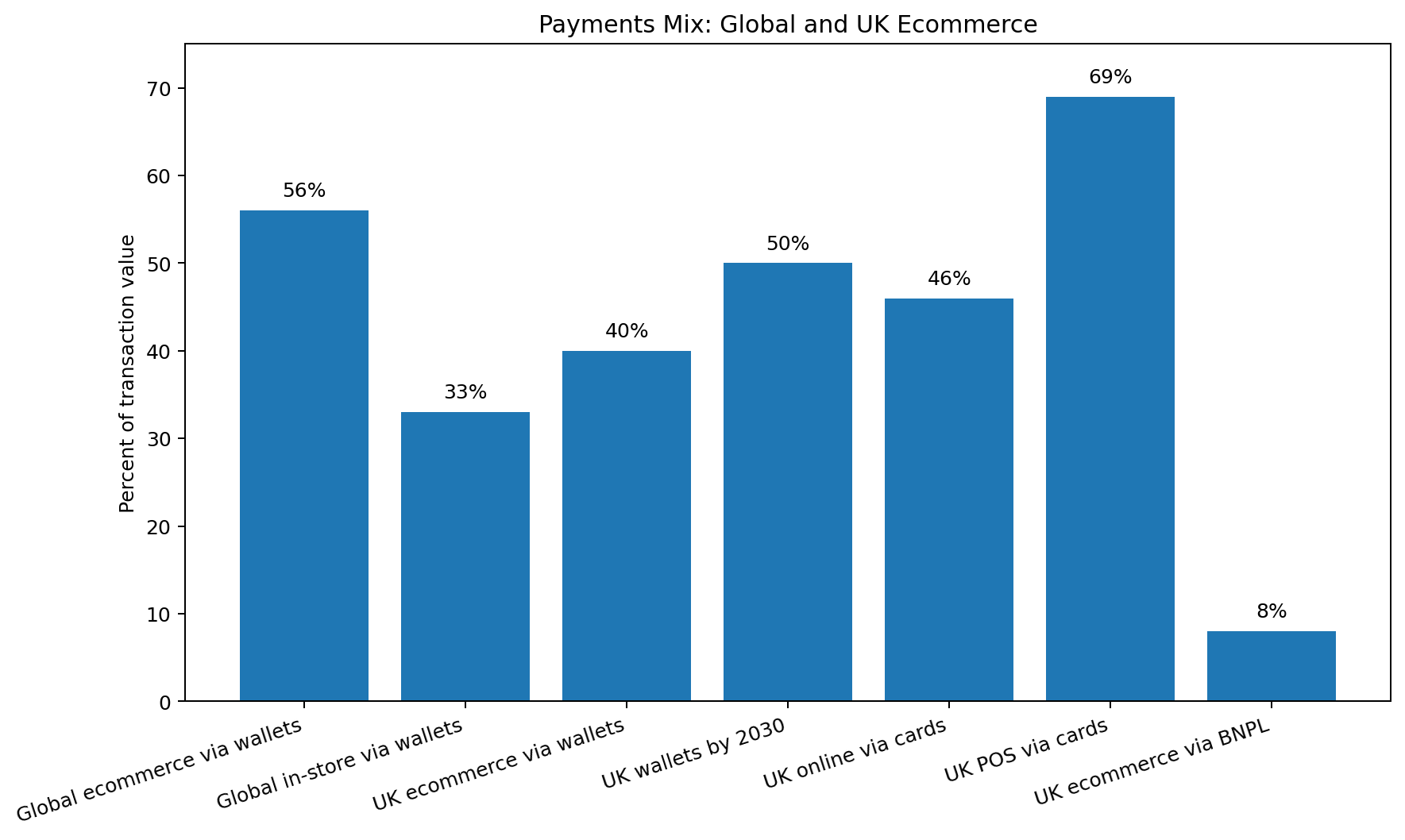

Worldpay says digital wallets now account for 56% of global ecommerce transaction value and 33% of in store spending based on its 2026 Global Payments Report covering 63,000+ consumers across 42 markets. In the UK, digital wallets already represent 40% of ecommerce value and are forecast to reach 50% by 2030. Worldpay also says more than half of UK adults now use a digital wallet, while direct card use still accounted for 46% of UK online spending and 69% of point of sale spending in 2025.

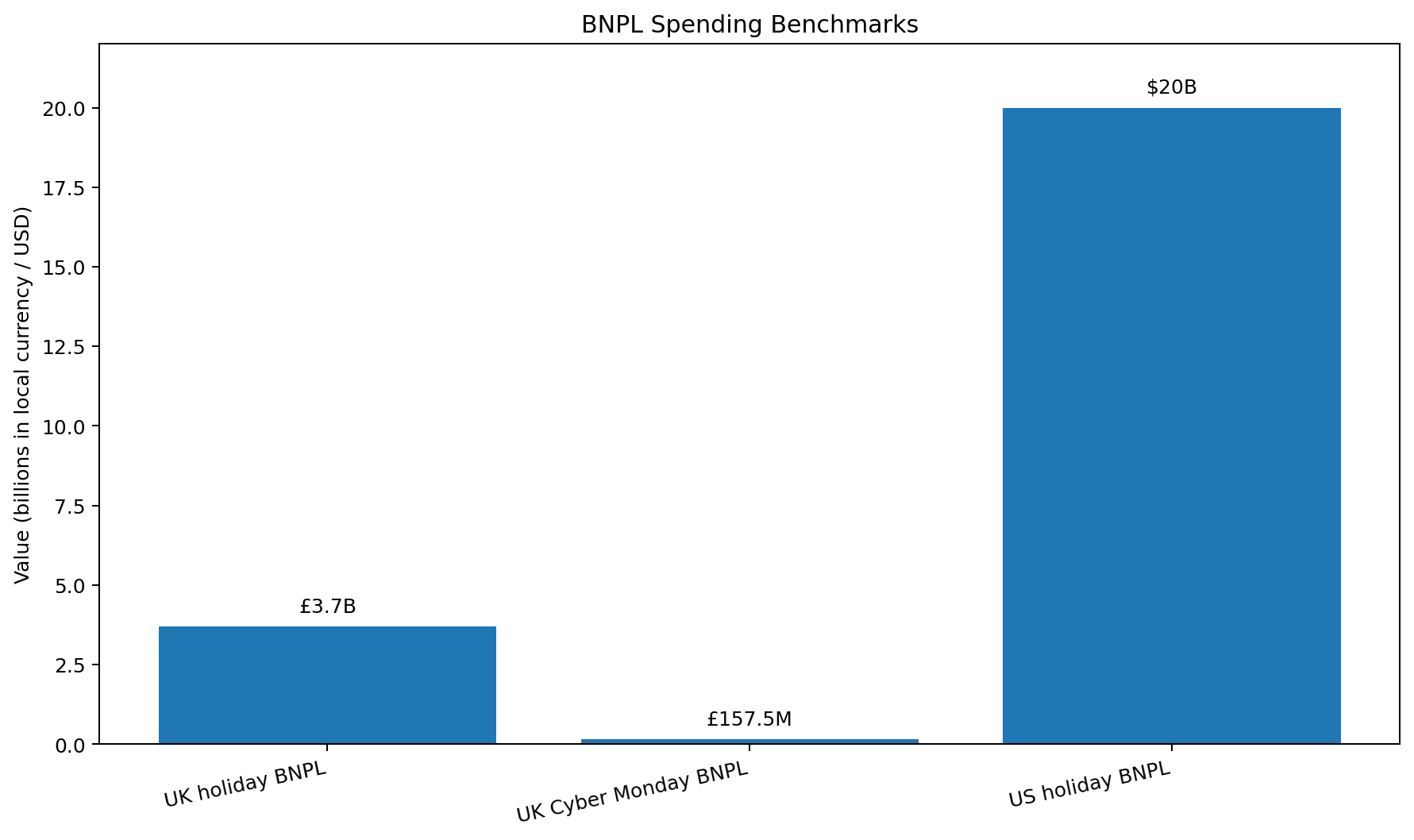

BNPL remains meaningful too. Worldpay says BNPL represented 8% of UK ecommerce value in 2025 while Adobe’s UK holiday report shows £3.7 billion spent via BNPL during the 2025 holiday season, up 2.2% year on year. Adobe also highlighted £157.5 million in BNPL spending on UK Cyber Monday alone, up 3.1% year on year. In the US, Adobe said BNPL reached a $20 billion milestone during the 2025 holiday period.

For ecommerce brands, this means payments are not just a backend detail anymore. They are directly tied to conversion, perceived convenience and trust.

AI is now part of ecommerce traffic, not just internal tooling

Another 2026 shift is how visibly AI is starting to influence shopping journeys.

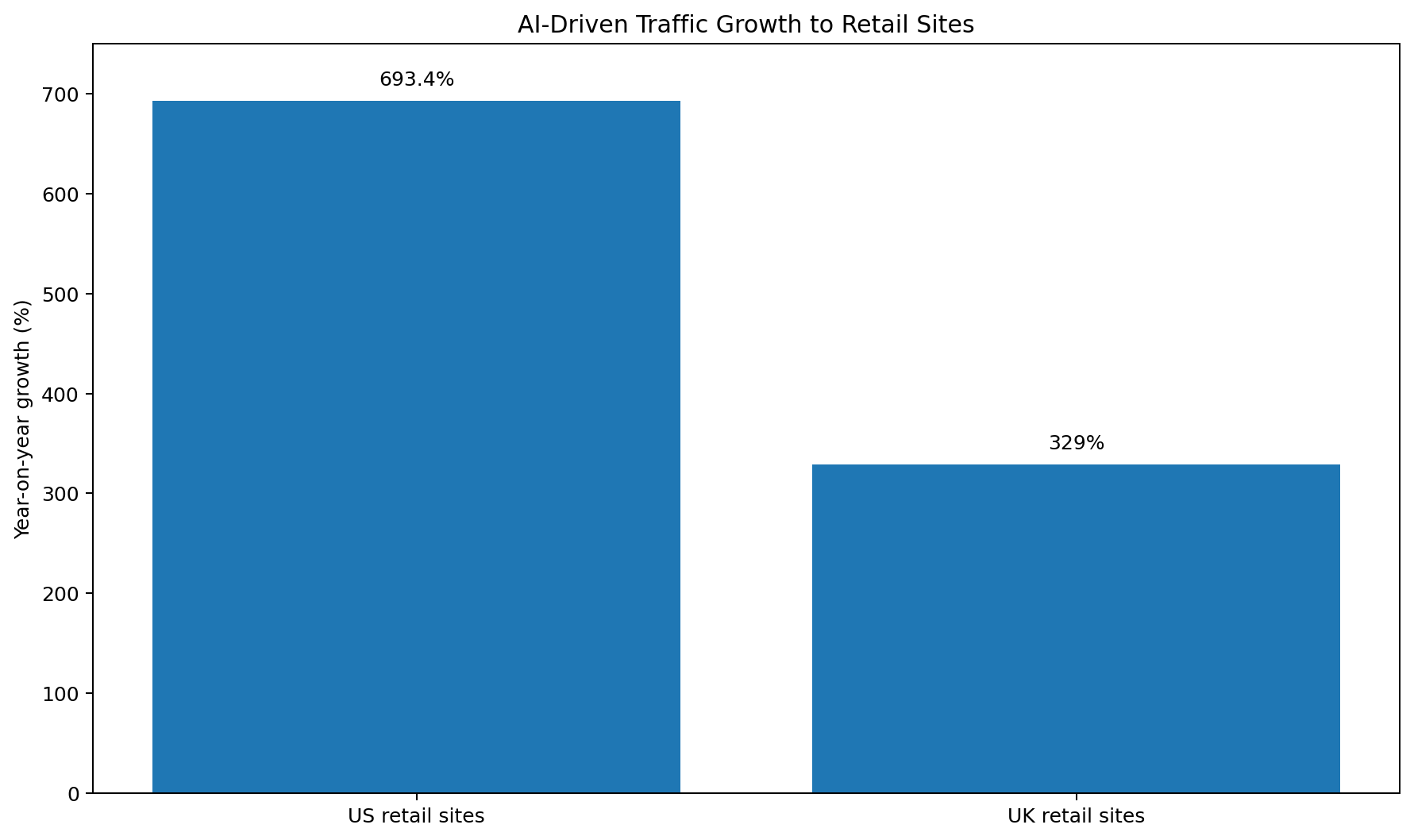

Adobe found that traffic from generative AI sources to US retail sites during the 2025 holiday season rose 693.4% year on year. In the UK, Adobe reported a 329% year on year increase in AI driven traffic to retail sites during the holiday period. This does not mean AI is replacing search or direct traffic yet but it does show that AI assisted shopping discovery is no longer hypothetical. It is already showing up in retailer traffic patterns.

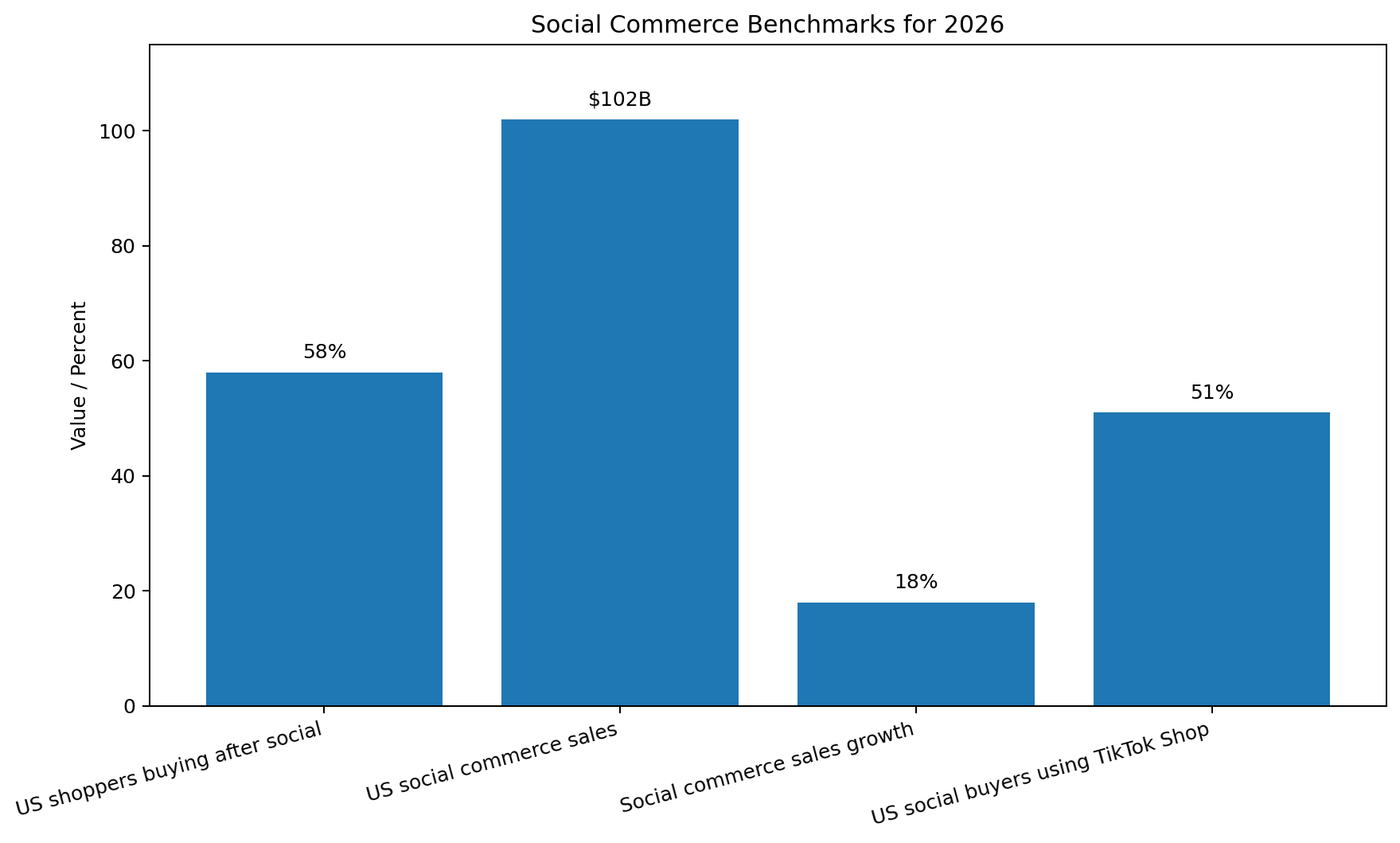

Social commerce is growing too. Sprout Social’s 2026 roundup says 58% of US shoppers bought something after seeing it on social media. It also says US retail social commerce sales are projected to surpass $102 billion in 2026, up 18% from the previous year and that about 51% of US social buyers are expected to use TikTok Shop in 2026.

Put together, those stats suggest the top of the funnel is getting more fragmented. Search still matters. Marketplaces still matter. But discovery is spreading across AI interfaces, social platforms and new in app commerce environments.

Conversion is still the weak spot

For all the growth in spend, ecommerce still leaks an extraordinary amount of revenue.

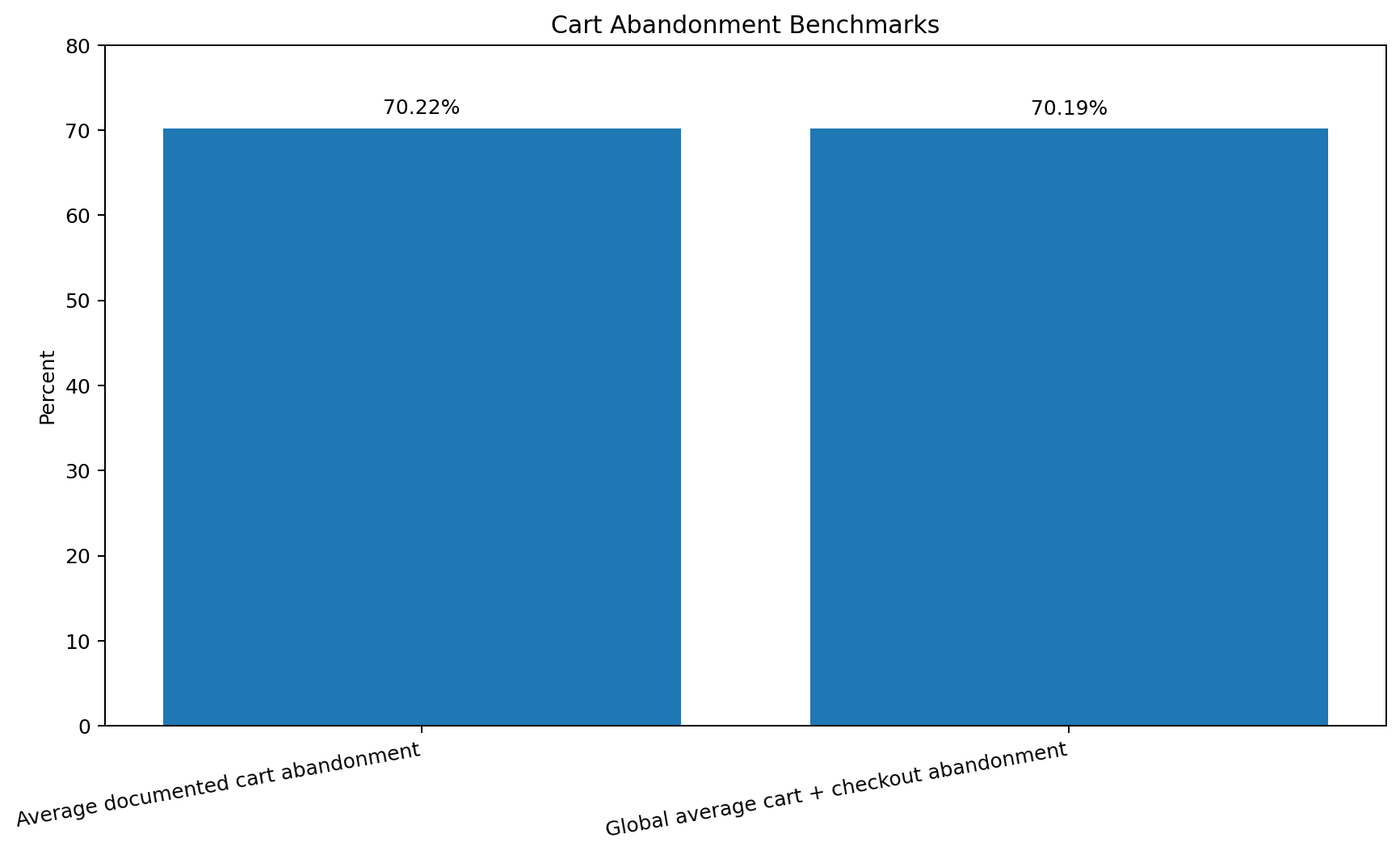

Baymard’s latest benchmark puts the average documented online shopping cart abandonment rate at 70.22% based on 50 different studies. Its cart and checkout research states the global average is about 70.19%. The message here is brutal... around seven in ten shoppers who add something to a cart still leave without completing the purchase.

That one stat explains why so many of the biggest ecommerce opportunities for this year are not just about acquisition in the slightest but it's all about fixing checkout, trust, shipping clarity, payment choice and returns.

The Latin America data supports this point. Nearly half of users say they would abandon a platform after a bad experience and most care more about clear prices and policies than any type of personalisation whatsoever. Worldpay’s 2026 analysis reaches a similar conclusion from a payments angle! Customers increasingly expect checkout to feel effortless and payment methods that shoppers actively use need to be supported as standard, not treated as optional add ons.

Ecommerce is getting bigger but measurement is still behind

One of the more overlooked 2026 themes is that official ecommerce measurement is still catching up with reality.

UNCTAD said in late 2025 that it had launched a new global database on ecommerce value, the first of its kind to consolidate available national estimates. It said ecommerce and digitally delivered services are among the fastest growing segments of the global economy with experimental figures indicating that ecommerce sales are expanding significantly faster than GDP. But it also stressed that most countries still lack robust statistics on online transactions, cross border digital trade and the fast expansion of social media based commerce.

This is a big deal. Ecommerce is now large enough to shape trade, tax policy, SME support and digital inclusion but policymakers and analysts are still working with incomplete visibility in many countries.

What the 2026 ecommerce stats really say

The numbers point to a market with a few very clear truths.

First, ecommerce is still growing at a healthy global pace with $6.88 trillion in projected sales and 21.1% of retail expected to happen online in 2026. Second, mobile is now the dominant device context for online shopping in many markets and in some periods it is already the majority of online spend. Third, payments matter far more than many brands admit with digital wallets now accounting for 56% of global ecommerce transaction value. Fourth, conversion friction remains enormous with cart abandonment still hovering around 70%. Fifth, the winners are increasingly the businesses that get basics right: fast mobile journeys, transparent pricing, reliable delivery, flexible payments and low friction checkout.

So yes, ecommerce is bigger in 2026. But the more interesting point is this that it is not just getting bigger. It is getting less forgiving.

Sources

https://www.shopify.com/uk/blog/global-ecommerce-sales

https://www.census.gov/retail/ecommerce.html

https://news.adobe.com/news/2026/01/adobe-holiday-shopping-season

https://business.adobe.com/uk/resources/holiday-shopping-report.html

https://www.worldpay.com/en-GB/insights/articles/what-63000-shoppers-just-told-us-about-paying

https://baymard.com/lists/cart-abandonment-rate

https://baymard.com/research/checkout-usability

https://sproutsocial.com/insights/ecommerce-trends/

https://unctad.org/news/stronger-statistics-measure-e-commerce-and-digital-economy